Where Will Nvidia Stock Be in 2030?

Shares of Nvidia (NVDA +1.40%) have risen by an impressive 380% over the past three years, fueled by the artificial intelligence (AI)-driven demand for its data center chips. However, the stock has been in a rut lately, rising just 12% in 2026, as of this writing.

The surprising thing to note here is that Nvidia stock is struggling to break out despite sustaining impressive revenue and earnings growth, driven by its continued dominance in the lucrative AI accelerator market. However, the world’s largest company by market cap can easily step on the gas once again.

In fact, Nvidia could witness a solid increase in its stock price by the end of the decade. Let’s see why that may be the case.

Image source: The Motley Fool.

Nvidia’s massive addressable market points toward solid long-term growth

Nvidia’s foundry partner TSMC recently noted that the global semiconductor market’s revenue could reach a whopping $1.5 trillion in 2030. The Taiwan-based foundry giant had previously anticipated $1 trillion in semiconductor revenue by the end of the decade. However, AI-fueled demand for chips led to a substantial upgrade to its guidance.

Today’s Change

(1.40%) $2.85

Current Price

$206.38

Key Data Points

Market Cap

Day’s Range

$206.03 – $208.24

52wk Range

$164.07 – $236.54

Volume

199.4K

Avg Vol

158.7M

Gross Margin

74.15%

Dividend Yield

0.14%

TSMC points out that AI and high-performance computing (HPC) chips will account for 55% of this lucrative opportunity. That puts Nvidia’s addressable opportunity in the AI data center chip market at an impressive $825 billion. For comparison, Nvidia’s data center revenue in fiscal 2026 (which ended in January this year) was $193.7 billion.

It is worth noting that $162.3 billion of its fiscal 2026 data center revenue came from sales of compute chips, while the rest was from networking components. So, there is still a lot of room for Nvidia to boost its data center chip revenue over the next five years, especially considering that it is the dominant player in this market with an estimated 80% share.

However, analysts believe that Nvidia’s AI data center chip market share may have peaked. That’s not surprising, as competitors Advanced Micro Devices and Broadcom have been making solid strides in this space. Additionally, Nvidia’s customers, which include both hyperscalers and pure-play AI companies, have been designing in-house chips to lower operating costs.

That’s why Nvidia’s AI chip market share is anticipated to decline to 75% this year. Let’s assume Nvidia continues to lose ground in AI chips for the next four years and ends up at just 50% market share in 2030; it can still generate more than $400 billion in data center chip revenue in 2030 (based on the $825 billion market size estimated above).

That’s almost 2.5x the data center compute revenue it generated in fiscal 2026. At the same time, investors shouldn’t forget that Nvidia’s data center networking revenue is growing at a much faster pace than compute. The company reported a 142% year-over-year increase in networking revenue in fiscal 2026 to $31.4 billion. It has started fiscal 2027 on a stronger note in this segment, with networking revenue tripling year-over-year to $14.8 billion.

Nvidia sells networking hardware, such as Ethernet and InfiniBand switches, and also offers software platforms to help developers program and manage networks. What’s worth noting is that demand for these networking switches is increasing rapidly due to AI and HPC. The InfiniBand market, for instance, is expected to clock 36% annual growth over the next five years, according to Mordor Intelligence. It could generate more than $164 billion in revenue in 2031.

Meanwhile, the data center switch market is projected to exceed $100 billion in revenue by 2030, according to Dell’Oro Group. Ethernet switches are expected to dominate this space. The pace at which Nvidia’s networking revenue is growing suggests the company is capturing a larger share of this space, which could pave the way for significant growth in this business segment over the next five years.

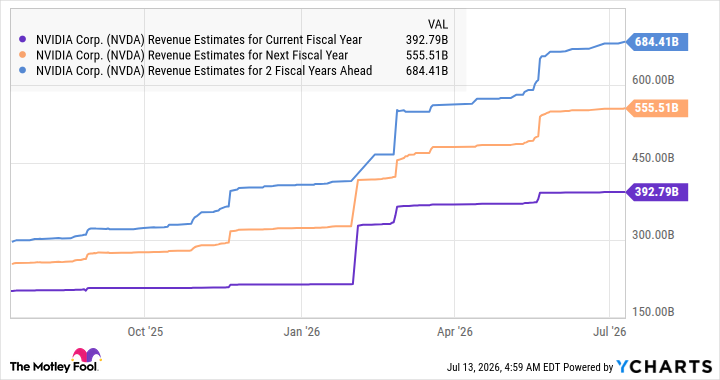

In all, Nvidia’s data center addressable opportunity, including both networking and compute, could surpass $1 trillion by the end of the decade. That’s why there has been a significant jump in Nvidia’s consensus revenue growth projections through fiscal 2029.

Data by YCharts

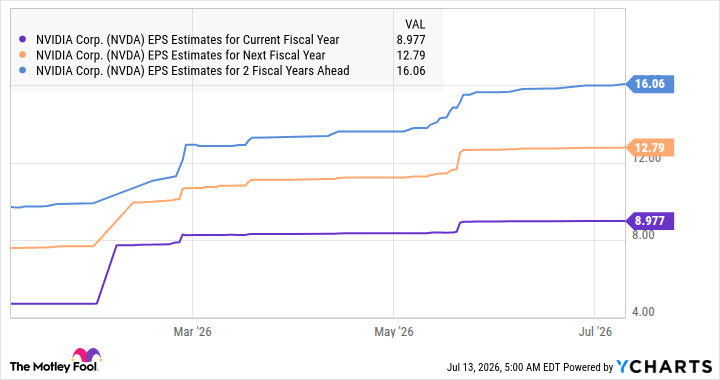

The company’s earnings growth potential suggests it can become a multibagger

Nvidia’s impressive top-line growth is all set to filter down to the bottom line. Analysts are projecting an 88% spike in Nvidia’s earnings in fiscal 2027 (ending in January 2027) to $8.97 per share. This will be followed by robust double-digit growth over the next two fiscal years.

Data by YCharts

Assuming Nvidia’s bottom line grows by even 15% a year in fiscal years 2030 and 2031, its earnings per share could reach $21.24 by the end of the decade (as its fiscal 2031 will end in January 2031). If this AI stock trades at 27 times earnings at that time (in line with the tech-laden Nasdaq-100 index’s forward earnings multiple), its stock price could reach $573. That’s almost 2.8x Nvidia’s current stock price.

As Nvidia trades at just 24 times forward earnings, investors are getting a solid deal on this growth stock, which they should consider grabbing, given the potential upside it could deliver through 2030.