This Wall Street Firm Just Placed a $725 Price Target on AMD Stock. Here’s Why It’s Wrong.

It is the job of Wall Street analysts to rate stocks and set price targets for them — figures that convey the direction they believe those stocks will take over the next year or so. While these are just predictions based on earnings forecasts, many investors put faith in these price targets when considering which stocks to buy. However, in my view, one recent analyst call on a widely followed chipmaker may have been a bit overzealous.

On Tuesday, KeyBanc raised its price target on AMD (AMD +0.37%) to $725 per share. That’s after a huge 140% rally this year that has lifted the stock to around $510.

Image source: The Motley Fool.

AMD’s stock has gotten ahead of its business

Since the AI arms race began, AMD has been behind. It’s starting to catch up in some respects, but it still commands only a small fraction of the AI accelerator market, which its rival Nvidia dominates. Furthermore, AMD’s business fundamentals don’t jibe with its current stock price.

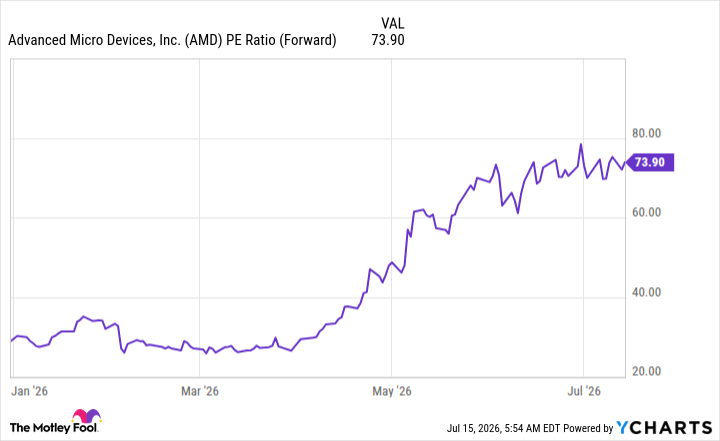

Right now, AMD trades for an expensive 73 times expected forward earnings.

AMD PE Ratio (Forward) data by YCharts

By comparison, Nvidia trades at a forward P/E of 23.6. That means that after this year’s growth is priced in, AMD would have to triple its earnings just to be valued at the same level as Nvidia.

That premise is a bit far-fetched, and there are a few reasons why.

One assertion you’ll hear AMD bulls make is that its profit margin could catch up to Nvidia’s, but I don’t think that’s possible. Over the past 26 years, AMD has never achieved a profit margin above 27%. Nvidia’s is more than 60% right now.

The difference stems from a few things. First, Nvidia’s products are best in class, which gives it the ability to charge premium prices for them. Second, AMD’s product focus is much wider, so it requires more resources to produce them. That will ultimately cap AMD’s potential profit margin, and even if it rises to 30%, that still wouldn’t be enough to make the stock reasonably valued at today’s prices.

Today’s Change

(0.37%) $1.87

Current Price

$502.81

Key Data Points

Market Cap

Day’s Range

$460.27 – $505.80

52wk Range

$149.22 – $584.73

Volume

876.8K

Avg Vol

35.8M

Gross Margin

47.09%

Next year, Wall Street analysts expect AMD’s revenue to grow by 56% to $77.2 billion. Assuming that AMD could boost its profit margin to a record-setting 30%, it would generate $23.2 billion in net income. AMD’s current market cap is $835 billion, so under that highly optimistic hypothetical, the stock would be trading today at 36 times next year’s earnings. For comparison, you can buy Nvidia’s stock right now for 32 times trailing earnings.

In that light, I don’t think the $725 price target is a great projection. I expect one of two things will happen with AMD’s stock. It could sell off to a more reasonable valuation. Or, its valuation may stay elevated, but if it does, Nvidia’s valuation will rise to a similar level because it’s growing faster and has stronger execution, in which case, Nvidia will again outperform AMD.

Regardless of what happens, I think Nvidia is the far better investment, and AMD shareholders should beware of hubris in the stock.