The top-performing 20 public banks with under $2B of assets in 2025

Community banks overcame a key challenge in 2025 by growing deposits, a task that had proved difficult in previous years. Across the entire universe of banks, deposits increased 4%.

Processing Content

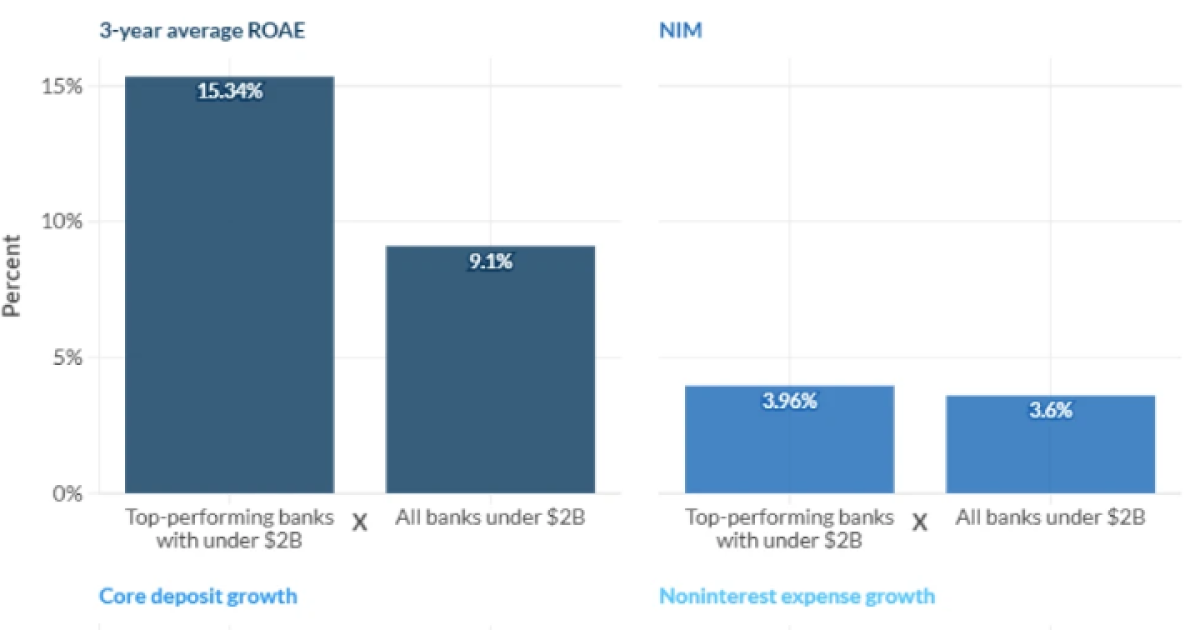

What separated the top-performing banks was their ability to maintain low overhead costs while growing efficiently. The banks were ranked by consulting firm Capital Performance Group based on their three-year average return on average equity, or ROAE, using data from year-end 2024.

Banks spent the last two years in a “painful competition to attract and retain deposits by paying higher and higher rates,” said Ally Akins, principal and marketing practice co-leader at Capital Performance Group.

“That pressure eased some in 2025,” she said. “More deposits at lower cost is a double win for bank earnings, and it was broadly shared across the industry.”

Matthew Prince, a business analyst at Capital Performance Group, said the banks that “genuinely earned their way to the top” shared several common strategies, including maintaining low-cost funding sources.

“Often through business checking accounts where customers park operating cash at little or no interest,” he said. “They also deployed that money into higher-yielding loans. They also kept costs lean and had few bad loans eating into profits.”

Prince added that ranking changes also reflected shifts in the interest rate environment. Banks with larger portfolios of floating-rate loans benefited as rates increased because loan yields rose while deposit costs remained more stable. Meanwhile, banks that had previously benefited from lower equity levels saw their ROAE metrics normalize as capital levels recovered and earnings growth slowed.

“Banks built for a higher-rate environment rose; the ones whose earlier rankings were partly borrowed from unusual circumstances fell,” Prince said.

The following are the top 20 public banks with under $2 billion of assets in 2025.

CNB topped the ranking of public banks with less than $2 billion in assets, although its first-place finish was also influenced by the accounting treatment of unrealized bond losses.

The Cheboygan, Michigan-based company reported an elevated return on average equity because unrealized losses in its securities portfolio reduced reported equity without affecting cash or underlying operations. The bank’s three-year average ROAE was 55.64%.

Despite that accounting effect, CNB continued to grow its loan portfolio, with net loans increasing 8.23% from the prior year, even as core deposits and total assets declined.

Pinnacle Bancshares ranked No. 2, though its return on average equity was boosted by an accounting quirk rather than stronger operating performance.

The $360 million-asset bank in Jasper, Alabama, held a sizable bond portfolio that lost market value as interest rates rose in 2022. Those unrealized losses reduced reported equity, which in turn inflated the bank’s return on average equity. Pinnacle’s three-year average ROAE was 35.21%, including a peak of 55.37% in 2023.

Solera National Bancorp held onto the No. 3 spot after another year of strong earnings growth.

The $1.5 billion-asset Colorado company, which operates through Solera National Bank, reported a 26.56% increase in net income in 2025. Its net loans-to-deposits ratio reached 72.61%, reflecting continued lending activity.

“While the results from 2025 will be difficult to beat, we have positioned ourselves for strong performance in 2026 and are very optimistic about the future of this bank,” board member Jordan Wright said in a statement.

FNB Bancorp slipped to No. 4 from second place despite another year of solid balance sheet growth.

The $1.16 billion-asset company, which operates 12 branches in southeastern Pennsylvania through First National Bank and Trust, increased loans 10.54% in 2025, led by commercial lending. Net income totaled $13.14 million, supported by growth in earning assets.

“These results continued to outperform peer benchmarks and position the bank for further margin and efficiency improvements as loan growth expands and operational initiatives continue,” President and CEO Daniel Schaffer wrote in the company’s annual letter.

Central Bank climbed three spots to No. 5 after posting one of the strongest loan growth rates among public banks with less than $2 billion in assets.

The Michigan-based company, which has approximately $487 million in assets and operates nine branches, expanded its loan portfolio by nearly 30% from 2024 to 2025. Its three-year return on average equity was 22.45%, while net revenue increased 13.02% year over year.

FFB Bancorp fell to No. 6 after topping the ranking of public banks with less than $2 billion in assets for the previous two years.

The $1.58 billion-asset company, based in Fresno, California, grew loans, deposits, assets and capital in 2025, but lower earnings and profitability weighed on its ranking. Net income came under pressure as noninterest expenses rose 11%, driven by higher operating costs and professional fees.

“While a 1.50% ROAA is strong by most bank standards, we are not satisfied with our 2025 results,” President and CEO Steve Miller said in a statement.

Professional fees increased 16% to $1.37 million, partly because of costs associated with a consent order issued by the Federal Deposit Insurance Corp. and the California Department of Financial Protection and Innovation related to the bank’s anti-money-laundering and counterterrorism financing programs.

BEO Bancorp fell two spots to No. 7 after net income edged lower despite continued balance sheet growth.

The $958 million-asset company, which operates Bank of Eastern Oregon across rural communities in eastern Oregon, eastern Washington and western Idaho, reported a 1.8% decline in net income from 2024. Even so, CEO Jeff Bailey said lower operating expenses and steady loan and deposit growth made 2025 a stronger year operationally.

“I can safely say that Bank of Eastern Oregon has never been in a better financial standing,” Bailey said in the company’s annual report. Net loans increased 5.6% to $612.6 million, while deposits rose 10% to $847.5 million.

Bailey said the year was marked by “tariffs and global political unrest” but noted that the bank’s loan portfolio remained stable and deposit growth strengthened its liquidity.

The $1.4 billion-asset holding company for Truxton Trust focuses on providing “financial advice to high-net-worth individuals, their families and their business interests.”

During 2025, the firm’s noninterest expenses increased by more than 18% year over year, partly due to higher personnel costs as the company expanded its workforce from 73 to 92 employees. “These folks joined every part of our business and should produce new revenue and depth in key service areas,” said Truxton Chairman Tom Stumb in the firm’s annual report.

The firm once again had the smallest net interest margin among the top performers of its cohort, instead pulling its profits from other financial services. Revenue from wealth services, which makes up nearly all of the company’s noninterest income, continued to grow by 6.8% from 2024 to 2025.

Bank7 climbed to No. 9 after posting loan and deposit growth that outpaced many of its peers.

The $1.96 billion-asset company increased loans 15.20% in 2025, while core deposits rose more than 14.18%. Mortgage lending income more than doubled from the prior year following the company’s 2024 acquisition of

“Our properly matched balance sheet has us well positioned to continue to take advantage of our dynamic geographic region,” CEO Thomas L. Travis said in his annual letter to shareholders.

Denali Bancorporation climbed seven spots to No. 10 after posting strong earnings and balance sheet growth.

The Fairbanks, Alaska-based company, which has $512 million in assets and operates through Denali State Bank, increased net income 18.2% and revenue 6.45% in 2025. Loan growth also remained strong, while the bank reported a net interest margin of 5.12%. Denali ended the year with a total risk-based capital ratio of approximately 15.3% and a three-year return on average equity of 19.53%.

Andover Bancorp, based in Andover, Ohio, made its debut in the top 20 after posting steady balance sheet growth in 2025.

The $587 million-asset holding company for Andover Bank reported a net interest margin of 2.94%. President Stephen Varckette said in the company’s annual report that three consecutive Federal Reserve interest rate cuts, combined with strong loan originations, helped support margin expansion.

The bank’s total assets increased 3.8% from the prior year, while deposits and loans grew 2% and 3.7%, respectively.

“Strong balance sheet growth was propelled by our strength in core transactional deposits that are highly valued in the banking industry,” Varckette said. “We also achieved record growth in small business loans for the third time in four years, with total originations exceeding the $30 million mark.”

Uwharrie Capital Corp climbed two spots to No. 12 after posting steady growth in both lending and deposits.

The $1.19 billion-asset company, based in Albemarle, North Carolina, increased loans 4.07% and core deposits 4.6% in 2025. Chief Financial Officer Heather Almond said the bank’s balance sheet remained strong, supported by a stable core deposit base and ample liquidity.

“The deposit base that we have remains strong and core in nature, supporting a solid liquidity position for Uwharrie,” Almond said. “We maintain our liquidity levels above regulatory expectations and access to multiple sources of funding allow us the ability to respond to changing market conditions as needed.”

Minster Financial posted loan and asset growth in 2025, while core deposits remained relatively flat.

The $802 million-asset company, which operates in western Ohio, was founded in 1914 and offers commercial lending and mortgage products through its banking subsidiary. The bank, which ranked 15th in its peer group for 2024 performance, saw core deposits increase 0.45% during the year.

Minster reported a total risk-based capital ratio of 16.85%, slightly below the 16.91% average among institutions in the ranking.

FFD Financial continued to benefit from a strong deposit base in 2025, with core deposits accounting for about 70% of total deposits.

The $891 million-asset company, which operates First Federal Community Bank in Ohio, maintained relatively low noninterest expenses, which totaled 1.94% of average assets during the year. The bank also maintained a larger loan concentration than many of its peers, supporting interest income growth.

FFD reported a net interest margin of 3.87%, supported by its lending activity and stable funding base.

CW Bancorp fell to No. 15 after asset and net income growth slowed in 2025, down from No. 6 the previous year.

The $1.48 billion-asset Southern California institution, which operates through CommerceWest Bank, remained profitable and maintained a total risk-based capital ratio of 18.86%, well above the 16.91% average among institutions in the ranking. The bank also saw noninterest expenses decline 6% in 2025 as expense growth moderated.

In the company’s annual report, CEO Ivo Tjan described the results as “solid” and highlighted the bank’s strong capital position.

“Our strong capital and liquidity position, combined with disciplined expense management and improving net interest income, position us well as we enter 2026,” Tjan said.

Woodsboro Bank climbed to No. 16 after posting higher loan growth and earnings in 2025.

The $455 million-asset Maryland-based institution increased loans 5.46% and net income 18.28% during the year, supported by higher interest income and continued lending activity. The bank offers commercial, mortgage and consumer lending products.

In its annual report, CEO Richard H. Ohnmacht said deposit growth was driven by “a combination of competitive products, attractive pricing and exceptional client service.”

Ohnmacht added that the bank ended the year with more than $20 million in cash and cash equivalents available to support loans and investments in 2026.

Mission Bancorp fell to No. 17 after ranking 12th in 2024, as higher operating costs pressured earnings despite strong loan growth.

The $1.9 billion-asset Bakersfield, California-based bank increased gross loans 13.2% in 2025, according to the company’s annual report. However, the expansion did not translate into higher net income as employee compensation, benefit costs, growth-related investments and interest rate-related margin pressure weighed on profitability.

President and CEO A.J. Antongiovanni said loan growth helped support margin expansion throughout 2025.

“That growth, combined with an improving yield curve, allowed us to increase net interest income in the fourth quarter and year-over-year despite the Fed’s continuing interest rate cuts,” Antongiovanni said.

Community Capital Bancshares, the smallest institution by assets in the top 20, posted strong lending growth in 2025 despite its size.

The nearly $280 million-asset Albany, Georgia-based company, which operates as the holding company for AB&T, increased net loans 10.4% during the year. The bank also reported a net interest margin of 4.45%, above the average among institutions in the ranking.

“Our results reflect record net income, improved earnings per share, stronger return on assets, a tighter efficiency ratio, and sound capital,” the company said in its letter to investors.

Citizens Financial Corp., based in Elkins, West Virginia, reported its strongest performance in the bank’s history in 2025, according to the company’s financial results, driven by record earnings and growth in commercial lending.

The $704 million-asset company reported net income of $10.2 million, an increase of $2.6 million, or 35%, from 2024. Return on average equity was 17.96%, while return on average assets reached 1.49%. The bank also reported a net interest margin of 4.07%.

The company focused on expanding commercial lending while keeping consumer lending relatively stable. Total loans increased by $10.3 million to $552.5 million during the year, according to the company’s results.

Deposit growth was supported by stronger local customer acquisition and a reduction in reliance on brokered funding. Brokered deposits declined by $14.2 million, while core deposits increased by $43.5 million.

Trinity Bank climbed from No. 22 to No. 20 after posting strong loan and revenue growth in 2025.

The $553 million-asset institution based in Fort Worth, Texas, increased net loans 12.51%, outpacing the 6.26% average growth rate among institutions in the ranking. Revenue growth reached 17.65% in 2025 compared with 2024, while total asset growth was 5.96%, slightly below the 6.05% average among peers.

The following table lists the rest of the top-performing public banks with under $2 billion of assets in 2025.