How financial advisors’ tenures tie into their compensation

Financial advisors are “grossly underpaid” in their first three years, but “grossly overpaid for the rest of your career,” according to one of them.

Processing Content

As part of a Financial Planning survey of more than 300 advisors who disclosed their total compensation anonymously, respondents offered revealing advice about pay for early-career professionals. Only one advisor used that specific industry axiom to explain what aspiring advisors should know. However, most warned young newcomers and career changers about the difficult early years of building a client base, noting the high barriers to entry that advisors must overcome to achieve an ultimately rewarding career.

Get a partner — on the job or in life

“It will be lower than you had anticipated, for longer than you had anticipated,” said one advisor managing between $500 million and $1 billion in client assets at a wirehouse. “Look to partner with a senior financial professional and share in that revenue in exchange for servicing the book of business. It not only provides stability as you grow your own book of business, but also teaches invaluable knowledge/training as you work with existing clients.”

Another advisor with a client base of similar size at a broker-dealer suggested that new entrants “have plenty of cash reserves for the early years (or a partner with an income)” to get through them. “It will be brutal for the first three years, then better, then great. Hold your breath and do not give up.”

Others discussed the trade-offs involved with compensation — especially the differences between working at a wirehouse, an independent advisory practice that uses a brokerage or a registered investment advisory firm that has no broker-dealer relationship. But even when taking those traditional industry distinctions into account, the respondents said that advisors can find success with any firm that aids them earn credentials, provides a clear career path and teaches them how to succeed in the business.

“Invest in yourself and in a firm that will invest in you,” one RIA-only advisor said. “Work hard to control client relationships over time. This will help you to increase your compensation and value to the firm over time.”

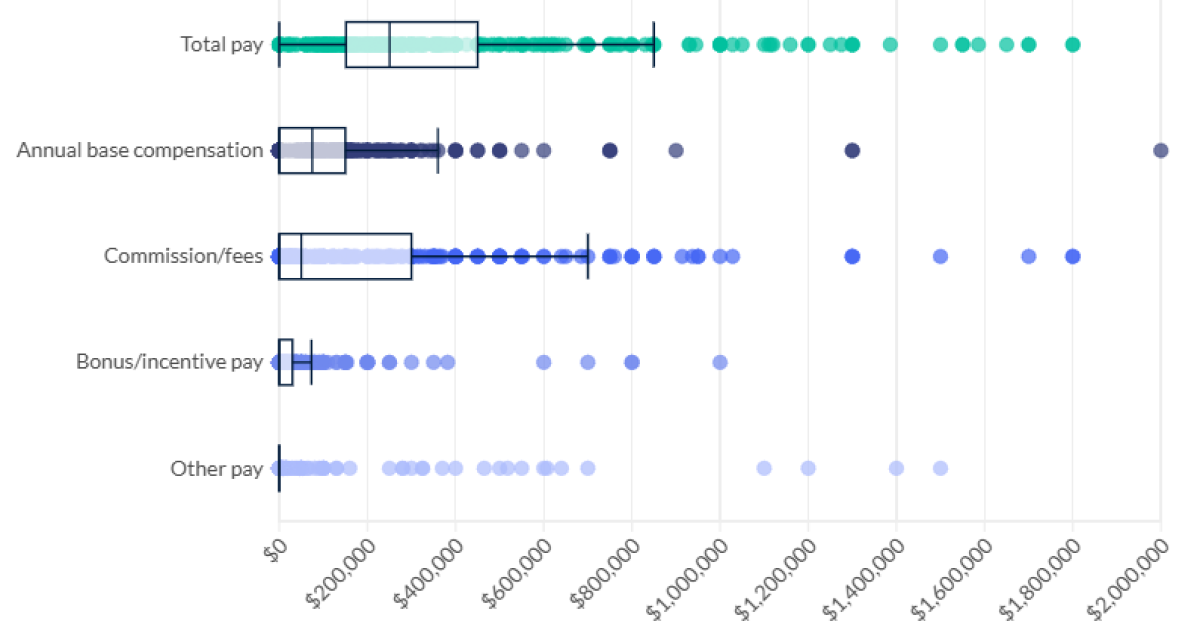

Advisors with the longest tenures and the most assets under management stretched the average pay of the group to more than $168,000 in base compensation, $224,000 in advisory fees or commissions, $47,000 in bonuses and $45,000 in other pay. But the median total compensation landed closer to that of the Bureau of Labor Statistics’ May 2024 calculation of $102,140 per year earned by personal financial advisors. Out of 352 advisors who participated in the online survey between March and April, 316 divulged their full compensation.

Factors tied to advisor pay

Similar to a controversial digital ad campaign by the CFP Board that some planners criticized for giving aspiring professionals an unrealistic image of the industry, those large figures contradict the fact that nearly three out of four rookie advisors fail to make it in the field.

Those aiming to break into a lasting career as an advisor must remember “the work and effort it takes to get there,” as well as the strong correlation between tenure and compensation, according to Jeffrey Czajka, the founder of consulting company Advisor Growth Solutions.

“If you look at income numbers, broadly speaking, if you just put them on paper, that’s pretty good,” Czajka said. “This isn’t necessarily a fault or a negative of the industry, but they take the 20-year numbers and they hang that in front of people, and it almost becomes an expectation of, ‘This is what I’m going to walk into.'”

Those compensation numbers could also vary a great deal based on the fee model, or whether an advisor is using a wirehouse or employee-channel pay grid or operating independently.

Among the advisors participating in the survey, 15% said they worked at a bank or wirehouse, 46% had a different broker-dealer affiliation, 11% were with hybrid RIAs that use a brokerage and 24% were with RIA-only firms. At least 40% of the group had worked in the field for more than two decades. One-third had tenures between 11 and 20 years, and 26% had been in the industry for a decade or less. And their region, tenure, job title, AUM and industry affiliations displayed a wide range of correlations with their pay.

An advisor’s personal AUM, time in the industry and holding senior-level roles within their firm demonstrated the strongest positive relationship with their total compensation. For example, 70% of the advisors managing at least $250 million in AUM, 65% of those with 20 years or more of experience and 67% of senior executives said they make more than $300,000 per year in total compensation. Region and industry affiliation showed some relationship with total compensation, but less pronounced.

Unlimited earning potential — with some important caveats

In their responses to the open-ended question, “What compensation advice would you share with professionals at the start of their career in financial planning?,” the advisors gave some hints about how those factors can enter into the pay equation.

“It takes a lot of effort to get the snowball rolling downhill, but once it’s rolling, there is no stopping it,” one advisor said. “You work in a career path with unlimited income potential. Let that guide you.”

Another suggested that early-career planners seek out roles that come with a base salary for the first three to five years, prior to earning compensation based on revenue production.

“That way you don’t have to starve like I did starting out, and once you’re established, you have a limitless income ceiling,” the advisor said.

The ability to make compensation less important at the beginning will pay off down the line, according to one advisor managing between $100 million and $250 million at a hybrid RIA.

“Focus less on compensation at the start outside of having enough to survive,” the advisor said. “Focus on getting the right credentials and education as well as ways to enter associations or networking events. The compensation will eventually come.”

That need for a clearly defined career track loomed large among the advisors.

“Make sure that the path to raises and promotion are clearly defined by objective benchmarks, and that the skills you are incentivized to develop align with the type of professional you want to become,” one advisor said. “If your income grows from meeting sales quotas, but you do not want to be a salesperson, then find a position where you are rewarded for other KPIs [key performance indicators].”

Others pointed out how important a team structure has been to their professional development.

“As someone in the start of my financial planning career, I HIGHLY recommend starting with a team and being associated with a senior advisor who has credibility and experience you can lean on,” one advisor said. “It takes the pressure off selling products to survive and allows you to learn and develop important technical and communication skills that are invaluable in this industry.”

With so much industry demand for quality advisor talent and many older planners expecting to retire in coming years, aspiring professionals may have more options available to them than they may think.

“Think about the space that you want to operate in, whether you want work for a large broker-dealer, a wirehouse, a mega RIA, a local boutique RIA, a financial planning only firm, etc., because they all compensate the advisor differently given their different variations in business models,” one advisor said. “Focus first on the type of clients you want to serve, the type of services you want to provide, and that should help you determine which business model fits what you want.”

Tough to make it in the business

Some potential future advisors, however, may never “get to what, on paper, looks like an extremely rewarding career,” noted Czajka, the former head of LPL Financial’s Independent Advisor Institute and the founder of a new professional network catering to early-career professionals. One of the difficulties revolves around how the industry’s training typically covers compliance rules, portfolio management, account onboarding and “how to do all these things that really have nothing to do with speaking to a stranger and convincing them that you’re the best person to help them get to their financial goals,” he said.

Another stems from the ongoing shifts toward comprehensive planning and advisory fees and away from the commissionable sales.

“The economic model of bringing an advisor into the industry is broken,” Czajka said. “We’ve changed how products and services pay advisors, but we haven’t changed how products and services get paid.”