HELOC, AI POS, LOS Tools; Pay Attention to Agency Changes; Housing Surplus?

One of the key selling points for an LO talking to a potential client about becoming a homeowner is the landlord/client relationship, which can go awry. (Pearl is the daughter of the short film’s director, by the way.) There are many reasons why renters aren’t owners, like, “can they not afford a residence,” or “are none available?” We recently learned that May new home sales slid to 580,000 (seasonally adjusted) and are down around 7 percent m-o-m and y-o-y. Sales of completed homes have declined for three straight months and are down over 30 percent since November. The supply of new homes for sale (496k) is now over 10 months, one of the worst in nearly 20 years. Median new home prices continue declining. All the while, most will say that no one seems to have any idea what our current national housing policy is. We have latched on to “affordability” but that has not been put into a policy. We’ve seen plenty of “trial balloons” about selling federal land, doing away with tri-merge, 40- or 50-year mortgages, and assumable mortgages. Nothing has stuck so far. There are small steps, like MISMO updating its mortgage insurance data standards to support VantageScore 4.0 and FICO 10T, helping firms prepare for new credit models. (Today’s podcast can be found here… this week’s ‘casts are sponsored by FICO. As the industry’s most predictive credit score, FICO Score 10T combines proven performance with deeper insight into borrower behavior to help support a stronger and more resilient housing finance system. Today’s has an interview with Sei’s Pranay Shetty on how purpose-built agents that handle borrower calls, process loan documents, do contact center QA, and monitor compliance are driving mortgage operations forward.)

Broker and Lender Software, Products, and Services

You can go ask ChatGPT how many hot dogs Joey “the Jaws” Chestnut put down at Nathan’s this year and it’ll tell you, no problem, but go ask that same LLM why a loan in your pipeline has been stuck for nine days and it’s got nothing, because it doesn’t know anything about your shop, your loans, your data. Inside Dark Matter’s LOS, Empower, the Ask Aiva assistant flips that script. Ask Aiva can’t tell you a thing about Joey, but ask it what’s outstanding on a file or where a loan stands, and it’ll pull the answer straight out of your Empower instance and let you click right into the source data and the logic behind it, so you can see exactly why it’s telling you what it’s telling you. The internet’s full of hot dog stats. Your loans are the part nobody else can see. Read it here.

The mortgage industry has officially reached the “our toaster has AI” stage, so it is probably worth asking what AI should actually do inside a POS. LenderLogix’s eGuide, The Mortgage Lender’s Guide to Evaluating AI-Powered POS Solutions, helps lenders cut through the hype and evaluate AI tools based on what really matters: compliance, transparency, borrower experience, workflow fit, and whether the technology helps loan officers work faster without losing the human touch. Grab the free eGuide here!

Figure’s latest whitepaper outlines why the future of equity-backed lending belongs to the infrastructure pioneers. This 2nd annual version highlights how Figure partners (a current network of 300+ partners) are outperforming their peers, based on HMDA data. The article argues that the long-term growth and future of the equity-backed lending market, like the Figure Flagship HELOC, will be dominated by tech-forward companies that leverage advanced platform technology rather than traditional, manual frameworks. The analysis also concludes that nearly a third (32%) of the entire national market’s growth over the last three years flowed through a lender connected to Figure’s infrastructure. Read about real partner case studies at scale and how today’s winners find volume. Preview it today: Figure Factor: Why the future of equity-backed lending belongs to the infrastructure pioneers.

Now Next Later is today at 10AM PT. Presented by Relcu, Jeremy Potter and Eric Lapin are joined by William Gillis of Plaid to discuss how open banking and consumer-permissioned financial data are modernizing mortgage lending. The conversation explores the growing role of cash flow and transaction data in credit decisioning, expanding access to credit, and what lenders should watch as open banking adoption accelerates.

The Chrisman Marketplace is a centralized hub for vendors and service providers across the industry to be viewed by lenders in a very cost-effective manner. We’re adding new providers daily, so check back often to see what’s new. To reserve your place or learn more, contact us at info@chrismancommentary.com.

Conventional Conforming Changes

Freddie and Fannie, with their lion’s share of applications, are still the “game to beat” volume-wise. So, when they say “jump” the industry replies, “How high?”. Some suggest that the Agencies are doing some things that aren’t so obvious.

For example, recently Fannie had a revision to the DU 12.1 Release Notes. This wasn’t a formal Fannie Mae announcement, rather a revision to the DU Version 12.1 Release Notes that was added; The original release notes were sent April 29th.

“DU Risk and Eligibility Assessment (added June 17, 2026) As part of normal business operations and prudent risk management, we regularly review and update the DU risk assessment based on the latest market conditions and loan performance data. These updates are intended to ensure mortgages are safe and sustainable both for homeowners and for Fannie Mae; and enable us to continue to provide a steady and stable source of mortgage financing. The DU risk and eligibility assessment will be updated, including a modification to DU’s minimum credit risk standards. We anticipate that these changes will result in a moderate reduction in the number of loan casefiles that receive an Approve/Eligible recommendation. Note: These updates will only apply to new loan casefiles created on or after June 27, 2026.”

On June 24, the FHFA proposed to rescind its existing “Duty to Serve Underserved Markets” regulation and replace it with a new rule. According to the FHFA, the proposed rule would enable Fannie Mae and Freddie Mac to better serve very low-, low-, and moderate-income families in the manufactured housing, affordable housing preservation, and rural housing markets through greater innovation and reduced administrative burden.

The proposal removes the existing framework of prescribed statutory and regulatory activities that the Enterprises must address in their three-year plans, including the related concepts of additional activities, “extra credit,” and the requirement that each Enterprise address a minimum number of activities, and replaces it with authority to take “any eligible action” consistent with the statutory duty to serve that has not been deemed ineligible by the FHFA by regulation or after case-by-case review.

The FHFA stated that the current approach may have incentivized a “compliance-centric” mindset that prioritizes satisfying granular regulatory benchmarks over meaningful market impact, and that it intends to encourage the Enterprises to focus on innovative, high-impact initiatives rather than a high volume of disparate, small-scale activities.

The proposed rule also: (i) revises the method for calculating median income to better address families in areas with concentrations of low-income families, particularly in rural areas; (ii) removes the existing restriction on subordinate multifamily liens to provide the Enterprises with expanded flexibility to finance multifamily properties; (iii) updates the approach to determining affordability for manufactured housing communities; (iv) expands eligibility for Low-Income Housing Tax Credit equity investments from rural areas only to all underserved markets; (v) removes energy- and water-efficiency-related regulatory activities consistent with Executive Order 14394; (vi) revises the evaluation and rating process to focus on whether the Enterprise met the needs of each underserved market rather than whether it met its self-identified plan goals; and (vii) relocates all Duty to Serve requirements from 12 CFR part 1282 to a new part 1283. The FHFA intends the regulatory changes to take effect by January 1, 2028. Comments on the proposal are due by July 24.

National MI Bulletin UW 2026-04 announced updates to the TrueGuide® reflecting changes to Construction to Permanent Commitment Period, effective June 6, 2026, now 18-month. Additionally, revisions to various manufactured homes requirements such as including application of GSE requirements, removal of certain limitations on single-wide MH, and guideline removal regarding insurance exclusion from delegated underwriting authority, effective July 10, 2026.

Pennymac posted Announcement 26-33 regarding Fannie Mae’s introduction of HomeStyle Refresh, a rebranded version of the HomeStyle Energy mortgage. Announcement 26-33 describes its alignment with “Refresh” rebrand and Delegated client’s allowance to follow certain HomeStyle Refresh (previously Energy) guidance.

Independent mortgage brokers partnering with UWM will now have access to two credit scoring model options for conventional loans: FICO and VantageScore®. By offering both FICO and VantageScore, UWM is providing brokers with added flexibility to evaluate borrowers’ credit history using multiple scoring models and choose the option that best aligns with each client’s individual scenario. To make it even easier, when brokers use UWM No-Cost Credit Reports, both models will automatically run. More details about credit scoring options and VantageScore benefits can be found here.

AmeriHome Mortgage is aligning with recent Selling Guide changes per Fannie Mae SEL-2026-05 and Freddie Mac 2026-6 addressing multiple topics. See AmeriHome 20260505-CL Product Announcement for details.

Grow your affordable lending business with new area median income limits that are now live in Fannie Mae’s Desktop Underwriter®, Loan Delivery, and other resources. The increased income limits expand access to loan-level price adjustment (LLPA) waivers and loan eligibility in over 84% of census tracts.

See the status for all your team’s project requests with new enhancements to Fannie Mae’s Condo Project Manager™ (CPM™). Now you can submit requests and track status in one place.

Pennymac announced that they will begin accepting GSE loans with appraisals in the Uniform Appraisal Dataset (UAD) 3.6 format, effective with loan deliveries on and after June 12, 2026. View Announcement 26-66 for details.

Capital Markets

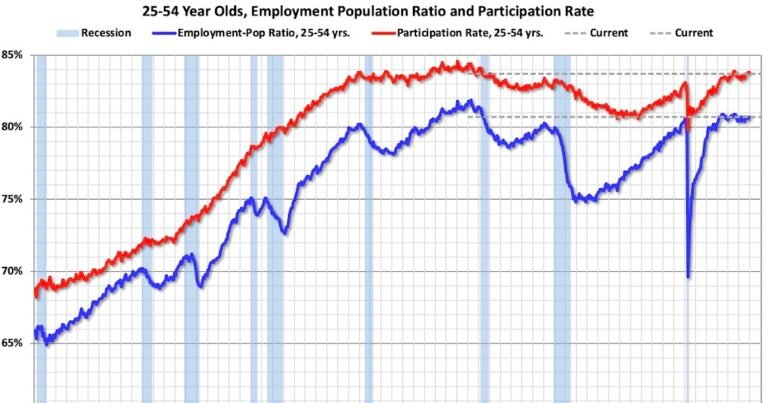

The dog days of summer are traditionally associated with the rising of the star Sirius, which was believed to bring heat, drought, and thunderstorms. During those conditions, people don’t do much, and certainly the rising of a star doesn’t move mortgage rates. But mortgage-backed securities and U.S. Treasuries ended the holiday-shortened week little changed but lower overall, as weaker-than-expected June payroll growth (+57k) and significant downward revisions to prior months were offset by an unexpected decline in the unemployment rate (down to 4.2 percent), driven by lower labor force participation. Employers remain cautious due to ongoing inflation concerns and consumer pessimism, with the largest job losses occurring in the leisure and hospitality sector. The mixed employment report supported shorter-term Treasuries and steepened the yield curve modestly. But things are active on the issuance front. June marked the fourth consecutive month of Agency mortgage-backed securities issuance exceeding $100 billion, with gross issuance reaching $118.5 billion (the strongest June since 2022) as overall mortgage production remained healthy despite a modest monthly decline. While refinancing activity continued to support issuance, its share of total production has fallen meaningfully since the first quarter due to relatively stable mortgage rates, leaving purchase originations increasingly important to sustaining supply. Conventional and Ginnie Mae issuance remained concentrated in 5.0 percent and 5.5 percent coupons, loan production continued to grow year over year, and, with refinancing expected to remain subdued, future issuance above the $100 billion threshold will likely depend on the strength of the purchase market. Today is light on economic news with the only thing scheduled are the non-rate moving Final June S&P Global U.S. Services PMI and June ISM Non-Manufacturing Index. Highlights from the rest of the week include May Trade Balance, May Wholesale Inventories, June FOMC Minutes, May Consumer Credit, June Existing Home Sales, and the quarterly refunding (consisting of 3-year, 10-year, and 30-year Treasuries). We begin the week with Agency MBS prices better than Thursday’s close by a few ticks (32nds), the 2-year yielding 4.11, and the 10-year yielding 4.46 after closing early Thursday at 4.49 percent, up 12-basis points over the course of the shortened trading week.