End of Iran ceasefire creates muni, UST losses

Bond markets saw losses Wednesday after President Donald Trump said the ceasefire with Iran is over and more strikes may be forthcoming. Equities ended mixed.

Processing Content

Muni yields were cut one to seven basis points, depending on the curve, while UST yields rose one to two basis points.

Over the past several weeks, oil prices and Treasury yields have been less closely linked due to the ceasefire, according to Elaine Brennan, executive director of the public finance department at Roosevelt & Cross.

With the ceasefire gone, oil prices are once again pressuring Treasuries, she said.

“When we look at the yield curve, we’re seeing a response that you would expect to see,” said Tim Iltz of HJ Sims, given spiking oil prices and geopolitical uncertainty.

Prior to the end of the ceasefire, the muni market had become somewhat inured to news from Iran, with little reaction to headline-driven developments that led to whipsawing USTs.

Munis “don’t always follow [Treasuries] tick for tick, but we can only tighten up so much, and as they back off, we’re going to have to back off,” said Peter Delahunt, managing director and head of the municipal bond department at StoneX. “We’re a little less elastic than they are, so we lag on the down and lag on the upside, but we’re weaker as this on-again, off-again war in the Middle East continues to plague our markets.”

Investors Wednesday also received the minutes from the June meeting of the Federal Open Market Committee.

The minutes were “dissected pretty carefully,” said Ajay Thomas, head of public finance at FHN Financial, although they “will be viewed through a slightly different, more cloudy lens, if you will, based on what’s happening in the Middle East right now.”

Iltz expects news out of Iran to override other market conditions for at least the rest of the week.

“Uncertainty is not a friend to the market,” Thomas said. He predicts the market will remain volatile until investors get more information on the direction of oil prices, the length of the conflict between the U.S. and Iran, and the Fed’s plans for interest rate policy.

Supply was just under $3 billion Wednesday, according to J.P. Morgan, as the weakness in the market did not disrupt deals.

Issuance this week, a more manageable $9.48 billion, is somewhat of a rebound after three weeks of fits and starts. The week of June 26 was the only full week during that period, sandwiched between two holiday-shortened weeks for Juneteenth and the Fourth of July.

This week is more of a return to normal, according to Jason Wong, vice president of municipals at AmeriVet Securities, as “everyone’s trying to catch up. Hopefully they want to issue this week, but I don’t know if it’s going to happen.”

Wong said he hopes muni ratios improve, as the front end has been “obscenely rich, so hopefully we get a correction in that.”

The long end, Wong added, is the cheapest part, and market participants may not want to go that far out at the moment.

The problem isn’t a lack of cash, said Thomas. Investors just got a lot of cash from July 1 redemptions, and they’re set to receive more on July 15 and August 1.

“We get the sense investors need to spend it, and are willing to spend it, but they’re gonna do so cautiously,” he said. “So we’re all kind of waiting in the market, seeing what might be an opportune time to get transactions in and out in a very orderly fashion.”

FOMC minutes

Federal Reserve officials’ concern about inflation grew, and while a “few” officials wanted to raise the fed funds rate target, they supported holding rates, according to minutes from the June meeting.

Upside risks to prices “remained elevated,” while risks to employment “moderated a bit,” the minutes showed. Several said price pressure was broad-based.

“Several” members said they didn’t see the policy as being restrictive, while a few saw it as slightly restrictive.

“There were no meaningful changes to the size or scope of this afternoon’s Fed minutes that captured Kevin Warsh’s first meeting as Fed chair,” said Will Compernolle, FHN Financial macro strategist.

“The Treasury market showed no discernible reaction to the release of the minutes, despite some noteworthy developments,” he said, including the breakdown on whether policy is restrictive. “The implication is that more participants believe policy needs to rise before it’s at neutral, regardless of whether energy costs pass through to underlying inflation.”

Additionally, Compernolle said, it appeared Warsh’s task force on “communication was ‘welcomed’ by only ‘some participants’ while ‘a majority of participants’ supported shortening the policy statement.”

“The minutes confirmed what the June 17 statement, dot plot, and Warsh’s presser portrayed,” said BMO Deputy Chief Economist Michael Gregory. “The Fed has a near-term hawkish bent, and further policy rate cuts are going to have to wait … perhaps for a long while. Although we reckon the Fed will keep rates on an even keel, a rate hike can’t be ruled out.”

“The Fed minutes confirmed the division among the committee members about what comes next for policy,” said Angelo Kourkafas, senior global strategist of investment strategy at Edward Jones. “Overall, the removal of easing bias represents a slightly hawkish tilt as there are concerns among policymakers over inflation being sticky and broadening at the same time as worries over the labor market are slightly receding. This is a higher‑for‑longer but not yet tightening stance.”

The panel is approaching “geopolitics as a macroeconomic inflation shock, which is why today’s developments are increasing the chance of rate hikes over the next twelve months,” he said.

Still, Edward Jones’ base case is a prolonged pause. “The Fed is unlikely to ease while inflation is moving higher, but there is not yet consensus among policymakers for tightening,” Kourkafas noted. “Even if the Fed delivers a single rate hike, we believe markets would likely view it as a mid-cycle adjustment, rather than the start of a renewed tightening cycle, provided inflation expectations remain contained.”

Joel Kruger, market strategist at LMAX Group, said, “While the FOMC minutes leaned hawkish, they contained few major surprises and offered little to suggest a rate hike is imminent.”

While officials tied persistent inflation to tightening, they showed “a willingness to keep rates on hold should price pressures begin to ease,” he said.

Jeffrey Roach, chief economist for LPL Financial, said, “The minutes suggest they had a ‘good family fight’ over the various scenarios under review.”

Still, the minutes show “some ambiguity” and suggest “several competing views on policy,” he said.

But the war with Iran will greatly influence policy, Roach noted.

“If we can tease out any forward guidance from the minutes, it would be the committee is working through a wide range of scenarios and will not commit to a specific scenario until the incoming data provides necessary clarity,” he said.

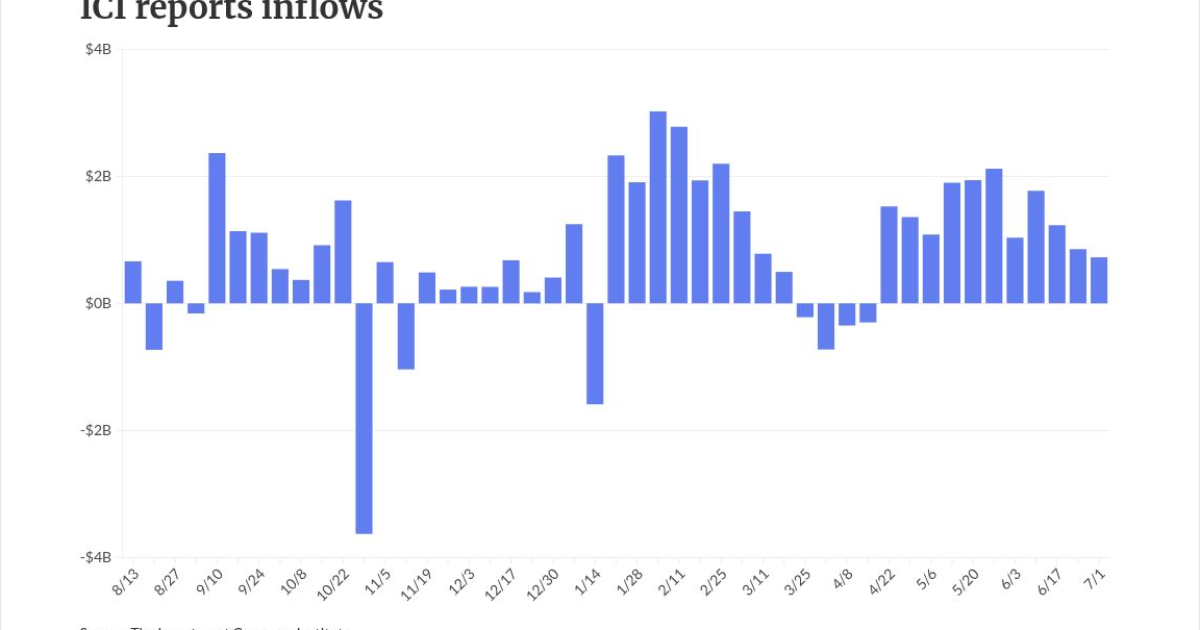

ICI data

The Investment Company Institute Wednesday reported inflows of $726 million for the week ending July 1, following $848 million of inflows the previous week.

Exchange-traded funds saw inflows of $1.794 billion after $432 million of inflows the week prior, per ICI data.

New-issue market

In the primary market Wednesday, BofA Securities priced for the Health and Educational Facilities Board of the Metropolitan Government of Nashville and Davidson County (/AAA/AAA/) $430 million of Vanderbilt University Tennessee educational facilities revenue bonds, with 5s of 10/2027 at 2.30%, 5s of 2031 at 2.66%, 5s of 2036 at 3.13%, 5s of 2041 at 3.51% and 5s of 2046 at 3.93%, callable 10/2036.

Ramirez priced for JEA $404.45 million of electric system revenue bonds. The first tranche, $161.3 million of Series Three 2026A bonds (Aa3/A+/AA/), saw 5s of 10/2028 at 2.53%, 5s of 2031 at 2.84%, 5s of 2036 at 3.23%, 5s of 2041 at 3.68%, 5s of 2046 at 4.05%, 5s of 2051 at 4.37% and 5.25s of 2056 at 4.50%, callable 4/2036.

The second tranche, $243.15 million of 2026 Series A subordinated bonds (A1/A/AA/), saw 5s of 10/2026 at 2.51%, 5s of 2031 at 2.88%, 5s of 2038 at 3.48%, 5s of 2041 at 3.73%, 5s of 2046 at 4.10%, 5s of 2051 at 4.42%, 5.25s of 2051 at 4.37% and 5.25s of 2056 at 4.55%, callable 4/2036.

In the competitive market, the New York State Thruway Authority (Aa3/A+//) sold $269.185 million of general revenue bonds, Series R, to BofA Securities, with 5s of 1/2047 at 4.18%, 5s of 2051 at 4.35% and 5s of 2056 at 4.56%, callable 1/2037.

The authority also sold $296.865 million of general revenue bonds, Series R, to J.P. Morgan, with 5s of 1/2033 at 2.85%, 5s of 2036 at 3.10%, 5s of 2041 at 3.55% and 5s of 2046 at 4.03%, callable 1/2037.