Community banks notch rare victory in housing package

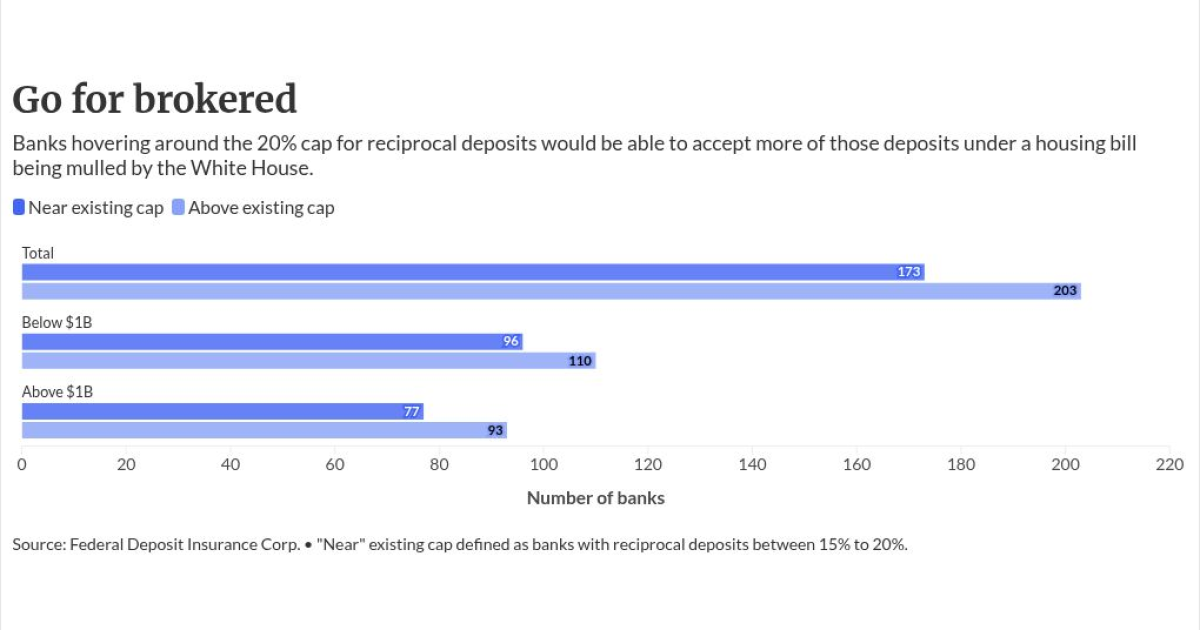

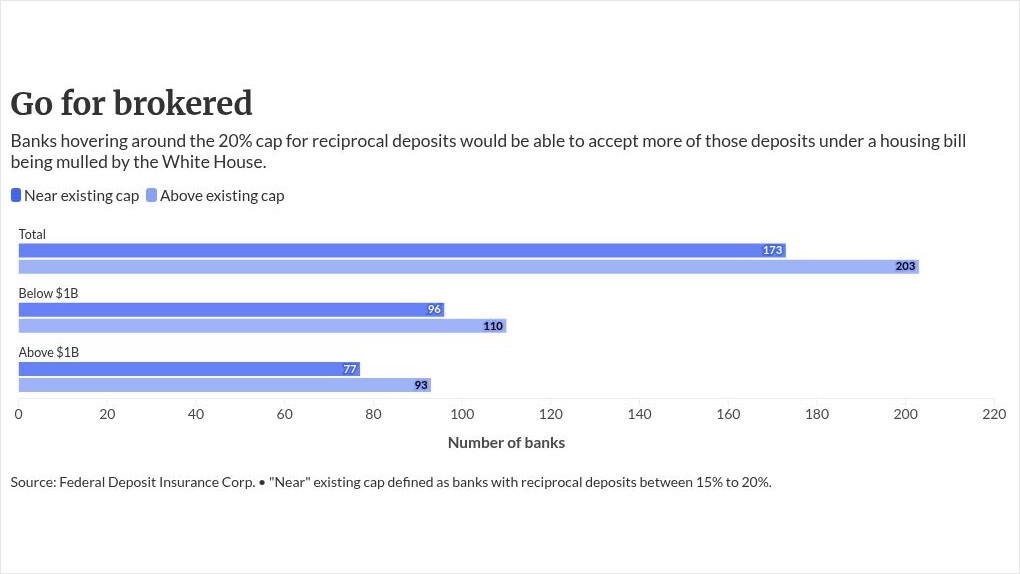

- Key insight: The housing package raises the threshold under which reciprocal deposits should be treated as regulated deposits rather than “brokered.”

- What’s at stake: The change means that more banks that aren’t considered “too big to fail” can attract local business and municipal deposits without the risk that those deposits will flee in times of stress.

- Forward look: President Donald Trump could still veto the bill on Friday, which would send it back to Congress to overturn. Alternatively, Trump could allow the bill to become law by doing nothing.

WASHINGTON — In a Congress that has been overwhelmingly focused on delivering for the crypto industry, community banks may finally get their own legislative win.

Processing Content

Tucked into the housing package is a provision that will make it easier for community banks to take larger deposits from local businesses, and even community governments. It’s a bright spot for small banks in a Congress that, despite being controlled by Republicans, hasn’t been as friendly to the banking industry, instead favoring

The package is expected to become law at midnight — if President Donald Trump doesn’t veto it first. Trump previously

Since then, Trump has complained about the housing bill being ineffective in addressing housing prices, instead saying that he prefers interest rate policy as a tool. Those comments suggest he may be building a rationale for vetoing the bill, and if he does, it’s unclear whether Republicans would overturn his veto — even though the bill initially passed with

Banks’ interest in the bill, rather than the housing supply features, centers on a

Regulators have

But after the Silicon Valley Bank regional bank crisis, when billions in uninsured deposits fled to the largest banks in search of safety, reciprocal networks that move deposits to maximize deposit insurance rather than interest rate return started to be viewed by policymakers on both sides of the aisle as a potential fix to that issue.

“Just knowing that there is space if you need it in a time of liquidity crisis,” said Christopher Williston, president and CEO of the Independent Bankers Association of Texas. “In those moments of crisis where more depositors are thinking about the safety and security and quite frankly the implicit guarantee that larger institutions have to know that these banks have larger capacity to accommodate larger insured balances through reciprocal relationships just helps them spread calm amongst their depositor base.”

The housing package provision would raise the threshold under which reciprocal deposits can be considered as not-brokered, up to 50% at the smallest banks. This gives small banks more leeway with regulators to put those reciprocal deposits on their balance sheets and allow them to go after local businesses and municipalities that are looking to place deposits larger than the $250,000 insurance limit.

In the near term, bankers say that the change would allow them to take larger deposits, and to continue to grow their business. Robert James, president and CEO of Carver State Bank, an about $115 million minority depository institution based in Savannah, Georgia, said the larger deposits could help his bank lend more in his community.

James testified in front of the House Financial Services Committee on the topic, and helped sway some Democratic votes and minds, according to two people familiar with lawmakers’ thinking.

“Over 60% of the residents of our headquarters census tract are living in poverty, our bank branch is kind of essentially surrounded on two sides by public housing projects, and so the consumers that we’re serving are very low-wealth individuals,” he said. “We use reciprocal deposit insurance products to bring in larger corporation deposits, or municipal deposits, or deposits from high-net-worth individuals who are … attracted by our mission and the impact that we have in these underserved communities.”

James said that, under the current rules, he’s had to turn down large deposits.

“If it’s a large corporation comes to me and says they want to do a $10 million deposit, I may say actually it would be better if you only deposited $5 million, and that’s because I’m trying to monitor and keep those ‘brokered’ ratios under where I’m not going to get additional criticism or scrutiny,” he said.

Jill Castilla, chairman, president and CEO of the about $440 million Citizens Bank of Edmond in Oklahoma, said that the change will allow the bank to add about $150 million in deposits to their reciprocal network.

“For us it’s just more of a perception issue, because our bank has very strong financials, and is in really strong and stable condition,” she said. “But for other banks, it does give them the ability to have those deposits on their balance sheet with customers that they originated without some kind of broker, which potentially can run into some restrictions.

“For us, it doesn’t have an implication or anything on FDIC assessment, but it does allow us to broaden our relationship with customers, and allows us to go after reading more corporate accounts and some public funds that we may have shied away from previously,” she said.