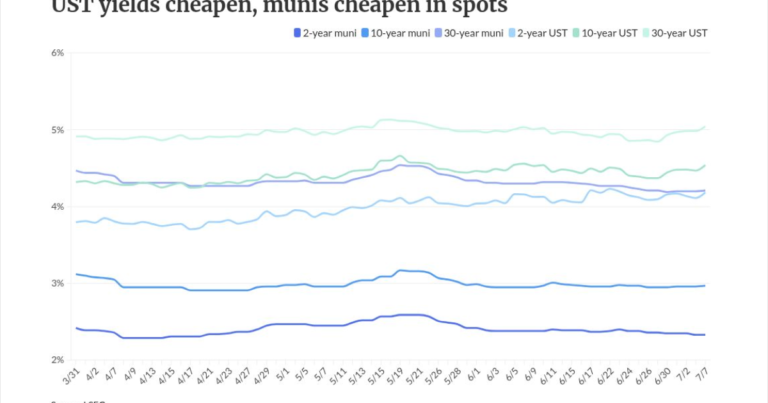

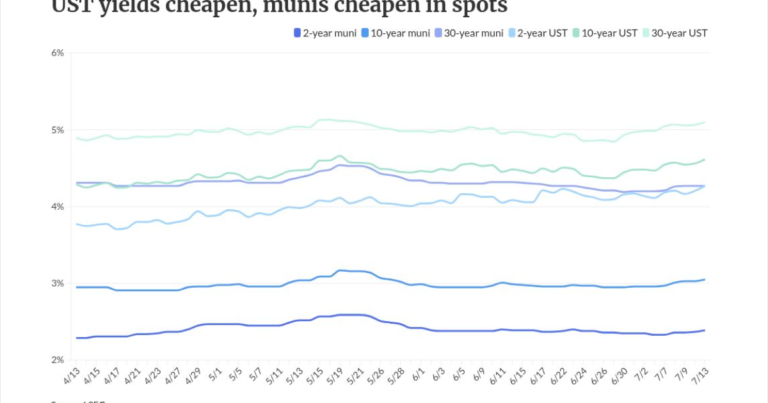

As Washington, D.C., plans revenue bonds, analysts focus on strengths

Bloomberg News

Washington, D.C., is preparing to bring $1.17 billion of bonds to market next week amid stresses related to a shrinking federal workforce, President Trump’s threats to take over the capital, and budget shortfalls, but many analysts say the city’s strengths outweigh the concerns.

Processing Content

The district is scheduled to price Tuesday $744.5 million of Series 2026A tax-exempt and $426.9 million of Series 2026B taxable income-tax supported revenue bonds. The former have serial maturities from 2039 to 2046 and the latter from 2027 to 2039.

The bonds are secured by a first lien on income and business franchise taxes.

Ramirez & Co. is senior manager and RBC Capital Markets is co-senior manager.

The district has experienced a whirlwind of change and instability since President Trump was sworn into office in January 2025. The bonds are rated Aa1 by Moody’s Ratings and AAA by S&P Global Ratings. Fitch Ratings, which hasn’t rated these bonds, rates the district’s issuer default rating AA-plus. The outlooks are stable.

Trump’s shrinking the federal workforce

The area’s federal employment is at a 25-year low, according to the Economic Policy Institute.

“The shrinkage of the federal government caused

With no further cuts in the federal government workforce expected, Mousseau added, “We are not worried about the city’s finances per se.”

Rising costs and flat revenue projections led the city council in late June to approve a budget that drew about $150 million from its reserves and $300 million in one-time funds to address a budget hole.

“The bottom line is that we’re facing a fiscal cliff. It took a lot of one-time funds to fix this year’s budget and we won’t have that option next year,” said City Council Member Brianne Nadeau, who last week proposed a new tax on high-earning residents’ investment and other passive income.

In early June, Trump threatened to end

“More worrisome [than the shrinkage of the federal workforce] is the president creeping into city affairs,” Mousseau said. “D.C. home rule exists because of the Home Rule Law passed in 1973, which gives Congress oversight of the federal district. So only Congress can change it. Any effort by the president to unilaterally remove it would be met by court challenges immediately, in our opinion.”

“Any change in the makeup of Congress this fall, and if we then have divided government, would most likely make this effort a non-event,” Mousseau said.

Muni Credit News Publisher Joseph Krist said, “To see how far the credit has come and the professionalism of the government versus [the] dark days [of the Marion Barry administration who left office at the start of 1999], makes potential intervention by the [Trump] administration all the more self-defeating. The impact of the DOGE cuts on the traditional professional functions continue to emerge daily. If the midterms go against the administration, it could help to restore some employment which was actually necessary.”

Both the job loss and the city’s weaker real estate market are real issues, Krist said. “Fortunately, the structure of the credit pledge behind the city’s debt and the strong coverage of the pledged revenues solidify the credit.”

Trump has a long history of threatening D.C.’s autonomy and some history of actually curbing it. He looked into taking control of the local police force in his first term and promised in his 2024 campaign to take over the city.

In August 2025, Trump renewed his threat to take control of the district’s government. Instead, he took control of the police force for the maximum allowed period of 30 days and sent in National Guard forces, with a stated purpose of helping with law enforcement, even though violent crime rates were the lowest they had been in decades, according to the Metropolitan Police Department.

The National Guard has remained in the city since. National Public Radio reported Tuesday the Pentagon said they will remain there at least until Inauguration Day 2029, unless the president decides otherwise.

Under the 1973 Home Rule Act, Congress can pass budget riders that regulate the city in various ways and overturn local laws, powers it rarely has exercised.

For Trump to legally take control of the city, Congress would have to overturn the Home Rule Act, which Senate Democrats would block.

The city’s financial shortfall in the spring was mainly due to increasing costs and not underperforming revenues, D.C. officials said. In April, Moody’s pointed to “stable revenue performance and balanced budget operations despite a weakened local economy” to explain raising the district’s outlook to stable from negative.

“Although the district’s local economy will continue to lag the U.S. because of federal workforce reductions and ongoing commercial real estate market weakness, the district’s very strong fiscal governance and prudent budget management will mitigate federal policy uncertainty and offset expected softer revenue during the next year,” Moody’s said in April.

The district has a highly educated workforce and above-average income levels and exemplary fiscal governance, Moody’s said in April. The district has among the lowest pension liabilities of any large U.S. city and has pre-funded its other post-employment benefits liability.

“These strengths offset vulnerability to federal government downsizing and a weak commercial real estate market, which have led to declines in income, sales and property tax collections,” Moody’s said in April.

In rating the bonds last week, Moody’s noted the broad pledge of the district’s personal and business income tax revenue results in a very strong coverage of maximum annual debt service at over seven times.

S&P noted many of the same positives as Moody’s. Revenues are expected to grow 3.1% per year 2026 to 2030, it said in its July report on the bonds.

The city has a deep and diverse economy, S&P said. In the near term, management expects to maintain its current strong levels of reserves through promoting growth and adjusting expenditures.

The city has a modest exposure to expected sea level rise but the city is trying to address flood risks in capital projects, S&P said.

Fitch noted similar positives.

“The district’s issuer default rating is capped at the U.S. IDR of AA-plus due to political risk from federal oversight of district budget decisions,” Fitch said.

The district’s history of revenue volatility has a “modest negative impact” on the implied rating, Fitch said in January.

The 2026A bonds are preliminarily subject to early redemption in 2036, according to Brad Friedman, managing director at Ramirez. The 2026B bonds are preliminarily subject to a make-whole redemption up to 2036.

The proceeds of the bonds will be used for projects in the district’s capital improvement plan. The Series 2026A bonds will refund bond anticipation notes. The Series 2026A will refund taxable bond anticipation notes.

PFM Financial Advisors and Phoenix Capital Partners are the district’s co-municipal advisors for the bonds.

Other underwriters on the deal are Bancroft Capital, Mischler Financial Group, BofA Securities, Morgan Stanley, Loop Capital Markets and Stifel.

Orrick, Herrington & Sutcliffe is the bond counsel.