Nvidia Stock Just Did Something for the First Time in 7 Years. Here’s What History Says Happens Next.

The artificial intelligence (AI) revolution turned Nvidia (NVDA +3.90%) into a household name virtually overnight. Since the public launch of ChatGPT in late November 2022, Nvidia stock has risen by 1,100% — making the company the most valuable business in the world.

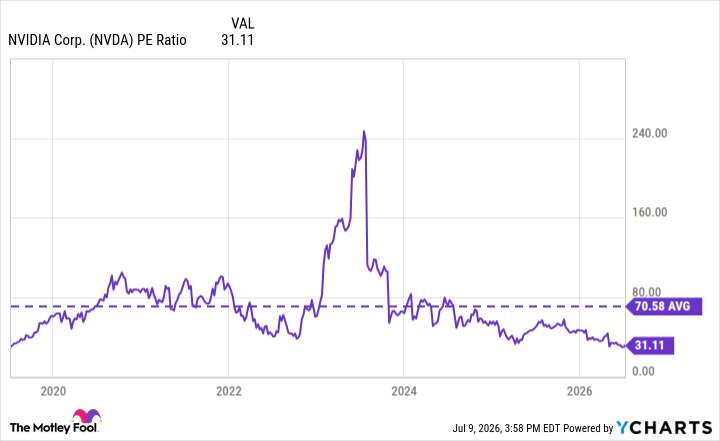

However, 2026 has been an entirely different story. Shares of the semiconductor darling have gained a modest 5% so far this year. With the stock’s parabolic rise coming to a halt, close observers may have noticed that Nvidia’s price-to-earnings (P/E) ratio is now at its lowest level in seven years.

Let’s dive into how this happened and what it means for an investment in Nvidia going forward.

Image source: The Motley Fool.

Nvidia maintains leadership in the AI chip stack, but investors worry about competition

Nvidia’s long roster of graphics processing units (GPUs) has helped the company maintain a central position in the hyperscaler AI chip stack. The company’s chips serve as the primary engines for both training large language models (LLMs) and running inference deployments at scale.

Major cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) and frontier AI labs such as OpenAI and Anthropic are leveraging Nvidia’s Blackwell GPU architecture and accompanying CUDA software ecosystem to build AI applications.

Skeptics highlight two main sources of risk when it comes to investing in Nvidia. On the macro side of the equation, some investors worry that AI hyperscalers could eventually moderate capex if returns on AI infrastructure investments prove slower to materialize. On the company-specific side, new accelerator architectures from Advanced Micro Devices and custom ASIC designs from Broadcom represent competitive threats that could erode Nvidia’s market share in certain data center workloads.

Today’s Change

(3.90%) $7.90

Current Price

$210.68

Key Data Points

Market Cap

Day’s Range

$201.91 – $210.87

52wk Range

$162.02 – $236.54

Volume

5.7M

Avg Vol

158.9M

Gross Margin

74.15%

Dividend Yield

0.13%

Where is Nvidia stock headed?

I think the concerns detailed above are legitimate and explain much of the compression in Nvidia’s P/E multiple. However, history offers a consistent pattern. The chart below illustrates that every prior period in which Nvidia’s valuation profile compressed was followed by a powerful and sustained re-rating higher once earnings confirmed the durability of growth.

NVDA PE Ratio data by YCharts.

Why is this? The reason is simple: Markets ultimately follow earnings trajectories, not sentiment.

What investors are currently discounting is the fact that Nvidia is expanding beyond GPUs into adjacent layers of the AI stack. This includes investments and strategic collaborations with companies like Nokia, Marvell Technology, Coherent, and Lumentum. Through these relationships, Nvidia is becoming increasingly embedded across high-performance networking, CPU offerings optimized for AI systems, and optical interconnects needed to stitch enormous GPU clusters together.

These moves expand Nvidia’s addressable market beyond general-purpose chips. As such, the company is in a position to create additional levers for revenue acceleration and compounded earnings. As Blackwell-driven revenue continues to materialize while diversification efforts scale, Nvidia’s earnings base should widen — setting the stage for meaningful valuation expansion.

All told, Nvidia’s current P/E levels appear to embed a degree of normalization after years of extraordinary expansion. This is important to understand, because it helps silence the idea that there is a fundamental deterioration in Nvidia’s underlying business.

Right now, investors are effectively pricing in the possibility that Nvidia’s growth will moderate from its peak rates more than acknowledging how the company’s absolute earnings power is positioned to expand. In turn, this creates a valuation setup that looks reasonable relative to historical trends, provided the company executes on its roadmap.

Adam Spatacco has positions in Amazon, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Broadcom, Coherent, Lumentum, Marvell Technology, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.