ClearBridge Emerging Markets Strategy Q2 2026 Commentary

tum3123/iStock via Getty Images

Market Overview

Emerging markets rallied in the second quarter as AI momentum among some of the largest technology names accelerated amid vigorous earnings results. The MSCI Emerging Markets Index rose 24.1% for the quarter, outperforming most global equity markets due to strength in South Korea, which surged 87.6%, and Taiwan, which jumped 48.9%. In an encouraging sign of broadening beyond AI, India rose 10.1%. Among EM’s largest markets, China (-6.6%) and Brazil (-8.2%), lagged, with the world’s second-largest economy hurt by a stagnant property sector and sluggish consumer spending while Brazil was impacted by a weakening currency and uncertainty heading into its general election.

From a sector standpoint, index performance was similarly concentrated with information technology (IT) up 73.3% and industrials ahead 18.2% while everything else underperformed. Consumer discretionary (-10.0%) was the worst-performing sector, pulled down by weaker consumer spending in China and negative sentiment over increased AI capex by Chinese e-commerce companies, while energy (-9.9%) lagged as commodity prices declined on hopes for a resolution to the Middle East conflict.

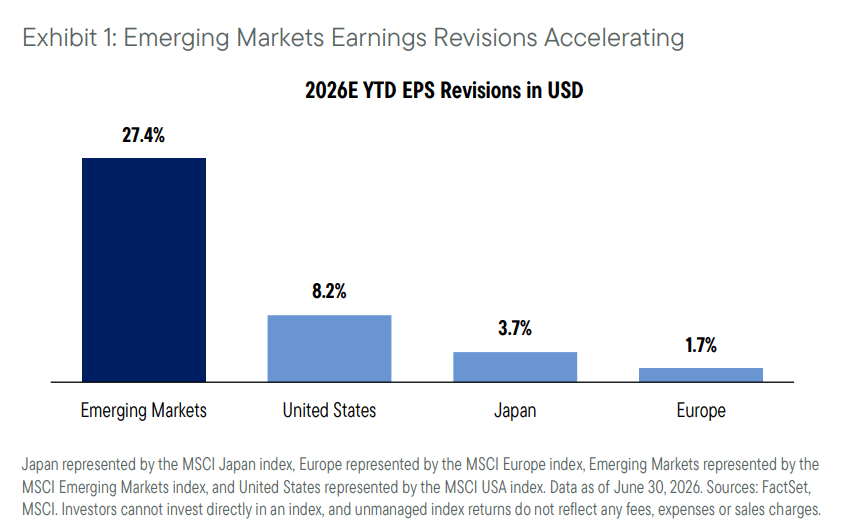

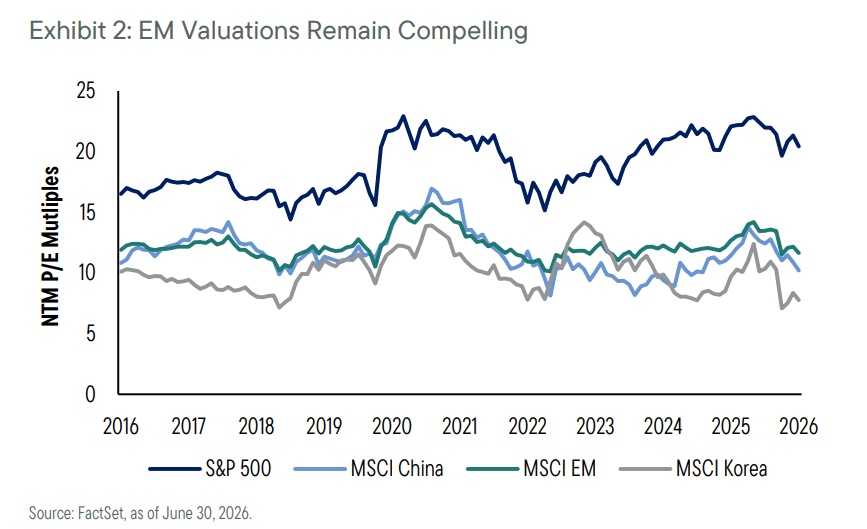

While we have rarely seen such concentrated performance in EM, it is important to note that the largest share price moves have been earnings driven and valuations remain reasonable. While SK Hynix shares soared 225% in the second quarter, net earnings for the South Korea memory provider grew even faster at over 320%. As of June 30, SK Hynix and Samsung Electronics traded at 6.8x and 6.2x next-12-month earnings, respectively, according to consensus estimates from FactSet, and Taiwan Semiconductor at a forward P/E of 21.2x. These multiples compare to a forward P/E of 12.2x for the MSCI Emerging Markets Index.

We are also encouraged by signs of wider market strength. Financials was the best-performing sector in June, reflecting healthy fundamentals in areas like India that are less exposed to the AI trade. While we would welcome more broadening going forward, we continue to have high conviction in our AI holdings due to their healthy profit profiles.

Performance Overview

The ClearBridge Emerging Markets Strategy outperformed its benchmark in the second quarter, boosted by positive stock selection in South Korea and an overweight to the country, with most of those contributions coming from our semiconductor exposure.

SK Hynix and Samsung (SSNLF) continued to benefit from an advantageous market for DRAM and NAND, and in particular high-bandwidth memory, as supply constraints amid high AI demand have supported higher prices. SK Square, a conglomerate that has a major holding in SK Hynix, was also lifted by the memory trend.

Taiwan Semiconductor (TSM) moved higher on pricing power and a healthy backlog due to its position as the dominant foundry for leading edge chips. Also in Taiwan, MediaTek saw encouraging results from its emerging AI accelerator chips business for customers including Alphabet, while Delta Electronics continued to benefit from strong demand for its power supply and thermal management products on the back of continued AI server buildout. Delta has broad global exposure with around 40% of its business in the Americas and is well-positioned as an approved supplier for GPU leader Nvidia.

Tencent (TCEHY) was lower on negative sentiment over higher AI capex spending, and particularly the pace of potential monetization of its AI investments. However, we still think that, as the owner of “super-app” WeChat, the company is a significant potential beneficiary from the rise of AI in China.

Chinese electrical equipment maker Sieyuan Electric saw a pause after strong recent performance as its capex-heavy industry takes time for capacity buildouts to come through. We remain positive on Sieyuan as longer-term AI infrastructure and electrical grid upgrade themes play out. China Merchants Bank was lower primarily due to a weaker retail consumer environment in China, which impacted its business as a consumer-facing bank. However, we believe the business remains fundamentally sound.

Gold Fields (GFI) was hurt along with other South Africa gold mining stocks as gold prices saw a sharp decline during the quarter. In addition, Gold Fields saw some further overhang as one of its mining licenses in Ghana, set to expire in 2027, is currently under review.

Not owning South Korea’s Samsung Electro-Mechanics was also detrimental as the stock rose more than four-fold on surging demand for its capacitors and packing substrates that enable AI servers and networking.

Portfolio Positioning

The Strategy added four positions during the second quarter while exiting another.

In Taiwan, we purchased Accton Technology and Elite Material. Accton is a high-quality compounder operating in network switches — an increasingly critical part of data centers as AI drives rapid growth in data traffic. We have confidence in the long-term story given Accton’s strong relationships with major customers and its efficient, asset-light business model. Accton is seeing growing participation in AI infrastructure, and we think continued upgrade cycles support robust long-term growth at attractive valuations.

Elite Material, a provider of copper-clad materials used in circuit boards, has transitioned from a cyclical electronics materials supplier into a structural enabler of AI infrastructure with a competitive advantage in technology and manufacturing consistency. As AI systems become more complex and performance sensitive, Elite’s products become mission critical, underpinning sustainable pricing power and high barriers to entry.

We also purchased Brazil oil and gas exploration and production company Prio (PTRRY). Despite the ceasefire, continued supply disruptions in the Middle East are likely to keep oil markets volatile, with risks skewed toward further price increases. We believe that the market is only partially factoring in the risk that oil prices remain higher for longer. Against this backdrop, Prio becomes an attractive portfolio candidate, with a free cash flow yield of between 20% and 30%.

Conglomerate SK Square further diversifies our South Korea exposure. We are positive on the company for two primary reasons. First, 98% of the stock’s net asset value is SK Hynix, where we have a positive view given the strength of the current memory cycle. Second, we believe SK Square can continue to reduce its holding company discount from ~45% today to a target of less than 30% by 2028. We believe the combination of these two factors leads to a positive backdrop for SK Square, the purchase of which we partially funded with a trim of our standalone SK Hynix position.

Although Indian IT services provider Tata Consultancy Services (TCS) delivered good results in April, highlighting strong deal momentum, expanding margins and AI-led services as a key growth driver, other industry quarterly results suggest that protecting the revenue base may prove challenging going forward. While TCS screens attractively on valuation relative to its own history, we believe a number of other Indian franchises, such as banks, also offer attractive valuations but with a higher conviction in recovery.

Outlook

While performance in EM has been relatively concentrated in recent months, we continue to see long-term positive drivers for the portfolio from several areas, in particular: China, India and IT. In China, we see a stabilization in macro conditions combined with market valuations that are still relatively cheap on a global basis. In India, while the market has underperformed EM recently, we see long-term opportunities in high-quality, domestic-focused companies that the market has overlooked.

Technology has been the key driver of EM year to date, with strong performance and momentum among semiconductor and AI-related industrial and IT stocks, primarily in South Korea and Taiwan. This strength has been earnings-driven, which has kept valuations in check, with memory names such as SK Hynix and Samsung Electronics trading at multiples well below emerging markets overall. We remain positive on the outlook for the IT hardware sector as we continue to see a supportive combination of growing global demand and constrained supply.

We continue to be mindful of market concentration risk and believe our investment process offers ways for us to manage this while maintaining dedicated exposure to secular AI growth trends. By owning our best stock ideas, drawn from a diverse range of countries and industries, we aim to unlock the potential that exists in emerging markets without taking excessive risk. The most visible result of this is avoiding large country-level mismatches relative to our benchmark. We also monitor portfolio beta closely, combining higher-beta companies that have outperformed due to AI tailwinds with lower-beta holdings in areas like health care and consumer sectors.

Portfolio Highlights

The ClearBridge Emerging Market Strategy outperformed its MSCI Emerging Markets benchmark in the second quarter. On an absolute basis, the Strategy produced positive contributions across five of the nine sectors in which it was invested (out of 11 total). The leading contributor was the IT sector, while the main detractors were consumer discretionary, communication services and consumer staples.

Relative to the benchmark, overall sector allocation contributed to performance. In particular, an overweight to IT, underweights to energy and materials, a lack of exposure to utilities as well as stock selection in IT supported results. Conversely, stock selection in industrials, financials, consumer staples and communication services detracted from performance.

On a regional basis, stock selection in South Korea and an overweight to the country drove positive performance while stock selection in China, Taiwan, Brazil and India was detrimental.

On an individual stock basis, the leading contributors to relative performance were SK Hynix, Samsung Electronics, MediaTek, Taiwan Semiconductor and Delta Electronics (DLEGF). The primary detractors were Tencent, Sieyuan Electric, Gold Fields, China Merchants Bank (CIHKY) and not holding Samsung Electro-Mechanics.

About the Authors

Paul Desoisa, CFA

Managing Director, Portfolio Manager

Colin Dishington, CFA

Managing Director, Portfolio Manager

Andrew Mathewson, CFA

Managing Director, Portfolio Manager

Divya Mathur, ASIP

Managing Director, Portfolio Manager

Robbie McNab, CFA

Managing Director, Portfolio Manager

Alastair Reynolds, ASIP

Managing Director, Portfolio Manager

Aimee Truesdale, CFA

Managing Director, Portfolio Manager

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.