Foreclosure calls surge as FHA relief programs expire

Foreclosure inquiries increased for a third consecutive quarter and hit their

Processing Content

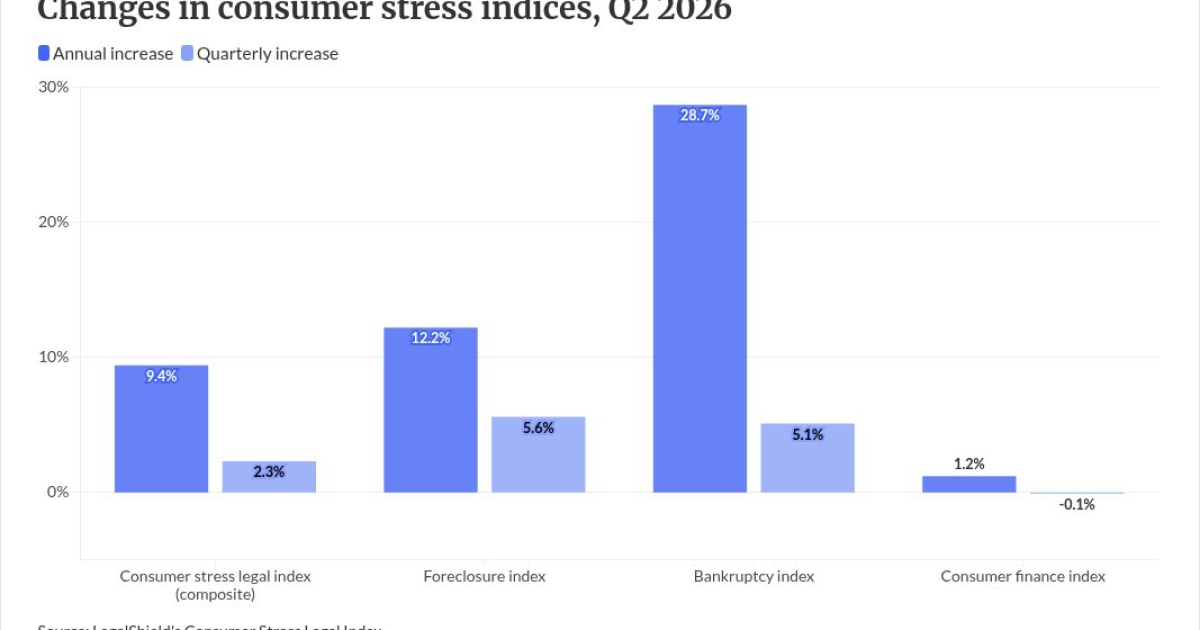

Its foreclosure index rose 12.2% year over year and 5.6% quarter over quarter to 52.5 in the second quarter this year. The index, a one- to two-quarter leading indicator of actual

“The second quarter shows foreclosure pressure building, with homeowners contacting attorneys in numbers we haven’t seen in years,” said Matt Layton, LegalShield senior vice president of consumer analytics, in a press release Tuesday. “Foreclosure, combined with the fastest-rising bankruptcy inquiries in our index, shows consumers are struggling to manage debt and can’t pay the bills.”

Federal Housing Administration loans and escrow were driving forces behind the jump in foreclosures. The FHA serious delinquency rate reached 11.5% in late 2025, its highest since 2021 and almost six times the conventional rate, according to the Mortgage Bankers Association. The increase aligns with the end of pandemic-era FHA relief options in September and new trial-payment requirements.

“The FHA relief programs expired three quarters ago, and we’ve seen foreclosure calls rise ever since,” Layton said. “We’ve tracked more than 36 million intakes since 2002. When we see the foreclosure index climb like this, actual filings tend to follow.”

LegalShield has also received calls from borrowers confused why their escrow has increased, which was usually a result of taxes and insurance, said Ben Farrow, LegalShield provider attorney, in the release.

Property taxes and homeowners insurance average almost 22% of typical

The bankruptcy index, which has historically led actual consumer bankruptcy filings by two quarters with a 0.98 correlation, rose every month in the second quarter, from 39.4 in April to 39.9 in May and 41.3 in June. The index increased 28.7% year over year in the quarter, the largest annual increase of the three indices.

“We are seeing an uptick in bankruptcy inquiries from middle-aged and older workers struggling to pay their mortgages, car payments and credit card balances,” said John Saltarelli, LegalShield provider attorney, in the release. “The strain is moving past the house. It is generally driven by the economy, higher prices and employer cutbacks that mean lost jobs or lower wages.”

The South was under more stress than any region, as its foreclosure and bankruptcy indices posted higher numbers than any of the four other regions.

The Midwest’s indices were split. Its foreclosure index saw the largest annual increase at 44.1%, while its bankruptcy index fell 10.1%.

The Northeast moved the opposite direction in both categories, with foreclosure inquiries down 31.5%, according to the report.