53% of Financially Strained Consumers Cut Nonessential Spending

Consumers are still spending, but many are doing it with less room for error.

That’s the central finding from “The Inflation Mirage: What Rising Spending Hides About Consumer Demand,” the latest edition of the PYMNTS Consumer Expectations Index, a PYMNTS Intelligence series based on a June survey of 2,028 U.S. consumers.

The report finds that headline spending growth can make consumer demand look stronger than it is. In April, nominal consumer spending rose 0.5%, but higher prices accounted for about 0.4 percentage points of that gain, while real purchase volume increased just 0.1 percentage points. In other words, consumers are often paying more for the same basket, rather than buying more goods and services.

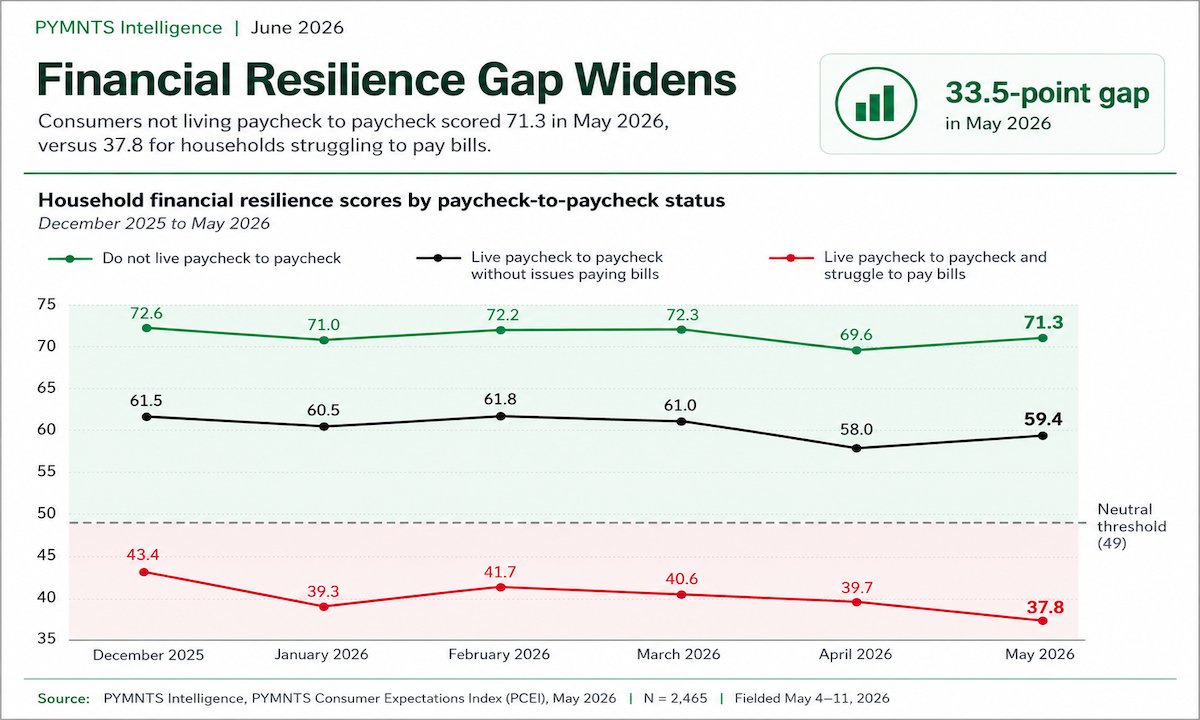

That distinction matters for financial resilience. Income was flat in April, while the personal savings rate fell to its lowest level since June 2022, according to the report. The overall PCEI score remained slightly positive at 53.6 in June, just above the neutral line of 50. But the index shows a divided consumer economy. Labor-market confidence remains relatively strong, while household financial capacity is weakening.

For many households, a steady job still acts like a shock absorber. It helps reduce the impact of higher prices. Yet a shock absorber only works when there is enough cushion left.

Key findings from the report show how uneven that cushion has become:

- 43% of consumers living paycheck to paycheck and struggling to pay bills could not cover a $1,200 emergency expense within one week, compared with 3% of consumers who do not live paycheck to paycheck.

- 68% of financially strained paycheck-to-paycheck consumers said their savings would last one month or less after missing work, and 45% said they had no savings at all.

- 54% of consumers living paycheck to paycheck and struggling to pay bills said essential expenses had risen “a lot,” compared with 22% of consumers who do not live paycheck to paycheck.

The optimistic view is that consumers are adapting rather than giving up. Many are changing how they spend, taking on occasional work or trimming nonessential expenses. Among the most financially strained consumers, 53% reported spending less on dining out, entertainment, travel and other nonessentials over the past year. That compares with 41% of consumers living paycheck to paycheck without issues paying bills.

The report also shows that not all paycheck-to-paycheck consumers face the same pressure. Those who can pay their bills still have a financial resilience score of 59.8, above the overall sample score of 57.1. Consumers who do not live paycheck to paycheck score 71.5. Those struggling to pay bills score 38.7.

For banks, lenders, merchants and payments providers, the signal is clear. Consumers have not disappeared from the marketplace. But many are more selective, more price-sensitive and more dependent on tools that help them manage timing, cash flow and emergency expenses.

At PYMNTS Intelligence, we work with businesses to uncover insights that fuel intelligent, data-driven discussions on changing customer expectations, a more connected economy and the strategic shifts necessary to achieve outcomes. With rigorous research methodologies and unwavering commitment to objective quality, we offer trusted data to grow your business. As our partner, you’ll have access to our diverse team of PhDs, researchers, data analysts, number crunchers, subject matter veterans and editorial experts.