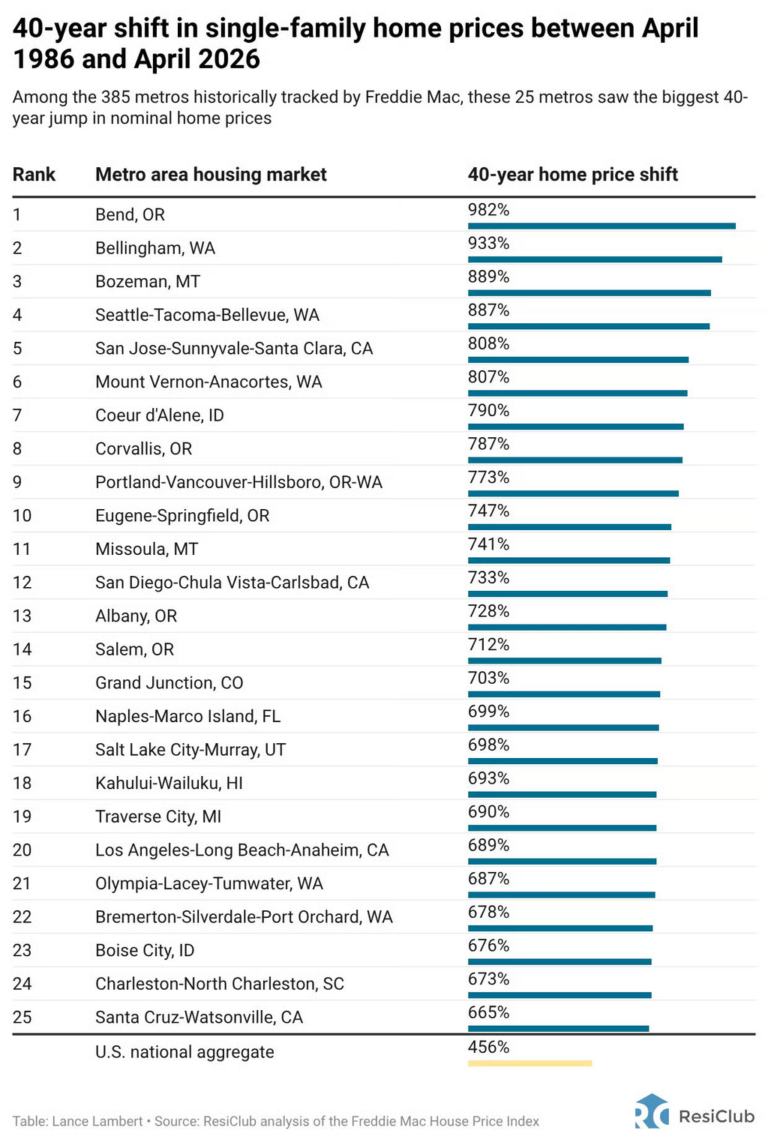

Brian Byrnes: The UK’s retirement savings gap is an advice challenge

The UK financial landscape is no stranger to a ‘gap’. The retirement preparedness gap as detailed by the UK Pensions Commission’s interim report, the gap in home affordability as a result of surging property prices over the last three decades, and the advice gap that sees just 9% of UK adults receiving regulated financial advice in the last 12-months.

Yet these challenges are too often discussed in isolation when, in reality, they are deeply interconnected. Encouragingly, the Pensions Commission begins to join those dots. It recognises that retirement outcomes are shaped by far more than pension contribution rates alone.

Those who reach retirement without owning their home often face significantly greater financial pressure in later life, while those without access to advice or guidance are less likely to understand how much they need to save, how their pension should be invested, or how to turn their retirement pot into a sustainable income when they stop working.

The retirement preparedness gap and the advice gap are particularly closely linked. The Commission’s analysis finds that many people are approaching retirement with savings that fall well short of what would be needed to sustain their desired standard of living later in life.

While much of the debate understandably focuses on contribution rates and policy reform, the Commission report also highlights a more fundamental challenge. We have built a system that increasingly relies on individuals making complex financial decisions, yet we have done relatively little to ensure they feel equipped to make them.

The task now is ensuring regulation evolves alongside the technology so consumers can benefit

If every person in the UK had access to a financial adviser throughout their working life, I suspect the retirement gap would look considerably smaller. The reality, however, is that the advice model has never had a practical solution to serve tens of millions of people at scale.

This is why the emergence of AI-enabled financial guidance and advice represents one of the most significant opportunities facing our industry today. For the first time, we can picture a future where personalised financial advice is accessible to almost everyone.

At Moneybox, we believe this has the potential to be genuinely transformative. Technology can dramatically extend the reach of advice services to millions of people. The task now is ensuring regulation evolves alongside the technology so consumers can benefit from safe, accessible and scalable support.

The urgency of that opportunity becomes clear when you look at some of the Commission’s findings. Take investment engagement. Despite investment returns accounting for up to two-thirds of a pension pot’s eventual value, 79% of defined contribution savers have never reviewed where their pension is invested.

We are asking people to make decisions that can shape decades of financial outcomes, often with little support

The picture at retirement is no less concerning. Pension freedoms have delivered greater flexibility and choice, but they have also transferred responsibility for managing longevity and investment risk onto individuals.

Nearly half of defined contribution pension pots are now fully withdrawn as cash, while 70% of pots worth less than £30,000 are accessed without any regulated advice or guidance.

Viewed through that lens, the retirement preparedness gap becomes far less surprising. We are asking people to make decisions that can shape decades of financial outcomes, often with little support and limited confidence that they are making the right choice.

This challenge is even more acute among the self-employed, one of the groups the Commission identifies as facing the greatest retirement risks. Sitting outside the automatic enrolment framework, only 4% of those earning solely through self-employment currently contribute to a pension.

Brian Byrnes: Britain isn’t bad with money — we’re just terrified of it

For many self-employed workers, the barriers extend beyond affordability. Their focus is, quite rightly, on running a business, managing cash flow and juggling competing priorities. Retirement planning rarely makes it to the top of the list.

Yet relatively simple interventions could have an outsized impact. Imagine a business owner receiving timely, personalised advice explaining how surplus company cash could be contributed to a pension, reducing a corporation tax bill while strengthening long-term retirement outcomes.

These are not especially complex strategies. Nor are they niche opportunities. The challenge is that the current regulatory framework makes it difficult to deliver this kind of personalised support at scale, leaving many people without guidance that could materially improve their financial future.

The Pensions Commission’s report is ultimately a reminder that retirement adequacy is not solely a savings problem

This is where technology and regulation need to work hand in hand. The tools increasingly exist to provide personalised financial guidance at scale. The challenge now is creating the framework that allows them to reach the people who need them most.

The Pensions Commission’s report is ultimately a reminder that retirement adequacy is not solely a savings problem. It is also an engagement problem, an education problem and, increasingly, an advice problem.

If every person in the UK had access to personalised financial advice throughout their lives, I suspect many of the problems identified by the Commission would look considerably less daunting. For the first time, advances in technology mean that ambition no longer feels unrealistic.

Brian Byrnes is director of personal finance at Moneybox