Is Bloom Energy the Next Nvidia?

Bloom Energy (BE 4.74%) has been one of the hottest energy stocks of 2026. And it hasn’t shown many signs of slowing down. Shares of the AI-power stock are up nearly 200%, and have grown ninefold since last July.

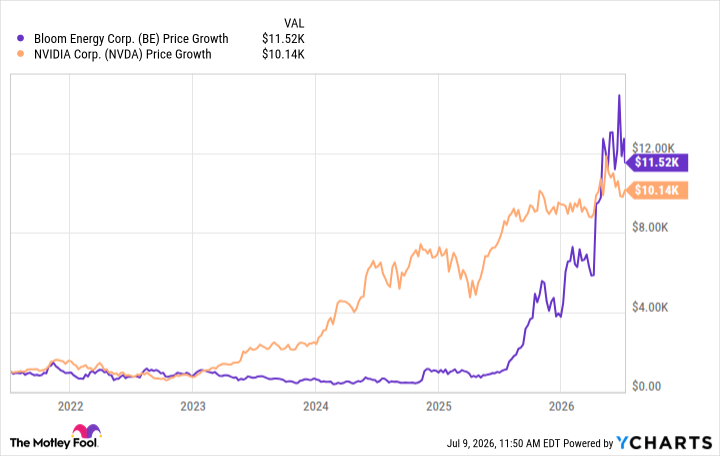

A comparison with the AI heavyweight Nvidia (NVDA +3.90%) can illuminate the shocking rate at which Bloom has exploded. Over five years, $10,000 invested in the chipmaker would have been worth about $1,500 less than the same investment in the fuel cell company.

Data by YCharts

This chart, however, says very little about each business. And if we press a little harder, we’ll see that, no, Bloom is not the next Nvidia — and that’s not a good thing for its bottom line.

Image source: Bloom Energy.

What Bloom is not

Bloom, like Nvidia, is capitalizing on a trend in artificial intelligence, one in which a power shortage is creating an opportunity for its fuel cell systems. Both companies are doing important material work for AI development. Yet their profitability couldn’t be more different.

Today’s Change

(-4.74%) $-12.17

Current Price

$244.85

Key Data Points

Market Cap

Day’s Range

$229.59 – $251.12

52wk Range

$24.04 – $351.28

Volume

722.7K

Avg Vol

12.2M

Gross Margin

31.08%

In the last 12 months, Nvidia has generated about $159 billion in net income; Bloom, by contrast, generated about $6 million. You can probably guess which has the better profit margins: Nvidia has a trailing-12-month net profit margin of about 63%, whereas Bloom’s is closer to 0.25%.

Of course, these are two very different businesses; one is capital-light, the other is capital-intensive. And that’s my point. Nvidia stock has surged on the back of extraordinary revenue growth and equally extraordinary profitability. Bloom, while improving its top line, has yet to demonstrate the earnings power to justify similar long-term investor enthusiasm.

This difference shows up in the companies’ valuations. Nvidia is surprisingly inexpensive, trading at about 23 times forward earnings. Bloom, on the other hand, trades at about 114 times the same metric — a very pricey valuation for a company that’s only recently become profitable.

What Bloom is

By stock performance alone, Bloom has already become the next Nvidia. Investors, however, should be asking whether or not Bloom can follow Nvidia’s path and report knockout earnings every quarter.

One reason it might not is the limit on its execution capacity. Bloom can only physically deploy so many fuel cell systems a year. Indeed, while U.S. data centers’ energy demand will, according to Bloom estimates, reach 150 gigawatts (GW) in two years, roughly double today’s levels, Bloom currently has the capacity to deploy about 1.5 GW to 2 GW annually. The company wants to scale up, of course, but right now it is still limited.

The valuation on Bloom is absurd right now, which is why I personally have been backing away from it. I fears that the market is misunderstanding the business — that Wall Street is overlooking the material constraints on its growth — which could set the energy stock up for a nasty correction. It’s not a strong buy for me right now, though I wouldn’t remove it from the watch list for a more favorable entry price in the future.