Three Quarters of Financial Firms See Identity Inconsistencies

Digital revenue has turned identity verification from a back-office control into a front-door growth issue for financial services firms.

The PYMNTS Intelligence report “When ‘Good Enough’ Isn’t Enough: Digital Identity Verification in the Age of Bots and Agents,” a collaboration with Trulioo, found that 76% of financial services firms earn at least three-quarters of their revenue through digital channels. That makes identity verification a larger business concern because every failed check, inconsistent result or slow onboarding step can affect growth, fraud prevention and customer experience.

For banks, FinTechs and other financial services firms, the issue is not that digital identity systems are failing outright. Most firms still express confidence in their know your customer (KYC) and know your business (KYB) processes. The problem is that digital dependence raises the cost of “good enough.” Identity systems now work like airport security for digital finance. They need to stop fraudsters without making legitimate customers miss the flight.

The report highlighted three data points that show how verification friction has become a business problem:

- The share of financial services firms that make at least three-quarters of their revenue through digital channels is 76%, increasing the impact of identity fraud, onboarding friction and inconsistent verification results.

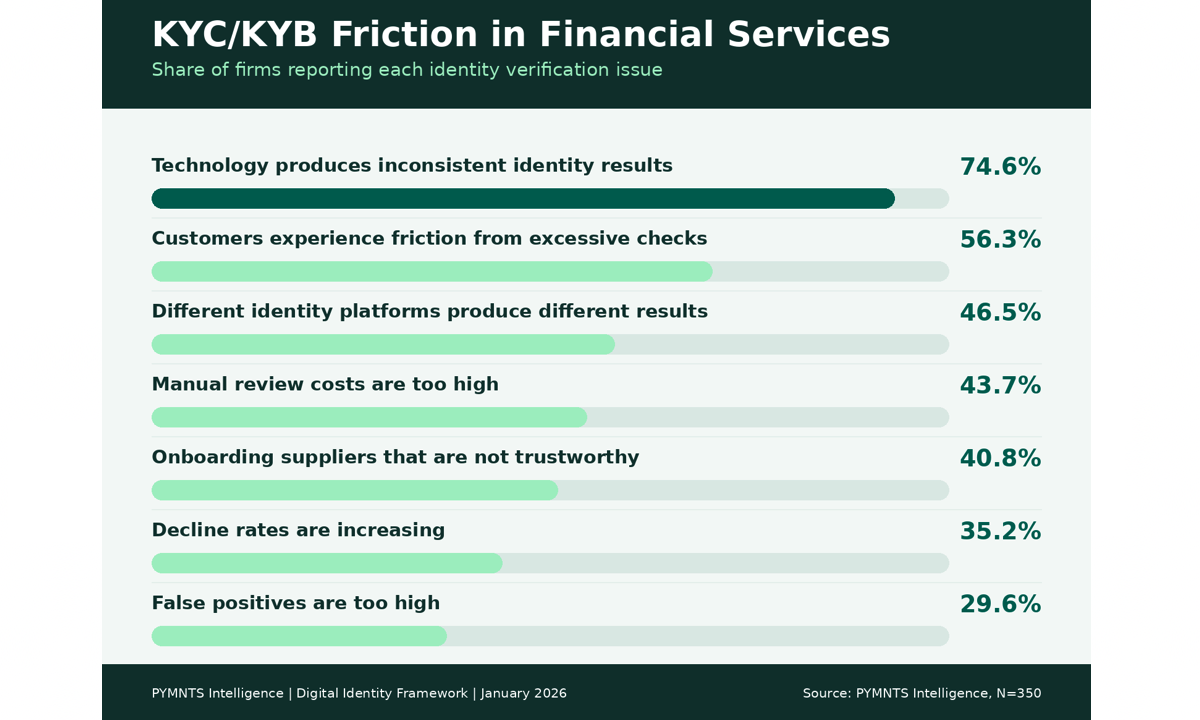

- Verification technology produces inconsistent identity results, according to 74.6% of financial services firms, while 56.3% said customers experience friction from excessive checks.

- The share of financial services firms that said identity processes prevent them from expanding customers, markets or geographies is 76.1%, while KYC/KYB failures produced revenue losses equal to 3% of revenue, or nearly $34 billion across the industry.

The findings suggest that identity verification now sits at the intersection of compliance, customer acquisition and revenue protection. Financial services firms are trying to serve more customers through mobile apps, digital onboarding and embedded financial products. At the same time, they face synthetic identity fraud, account takeover, stolen identity and adversarial bots. The more digital the business becomes, the more identity gaps can spread across the customer journey.

There is a positive angle in the data. The report revealed that 92.3% of financial services firms using a global identification platform said KYC/KYB has become easier over time. That suggests firms do not need to choose between stronger security and smoother onboarding. Better identity systems can reduce friction, improve consistency and help companies expand into new markets with more confidence.

The report also showed why many firms may delay change. Nearly 23% rated their KYC/KYB systems as best in class, and another 61% said they perform well with few issues.

Confidence comes from trusted vendors, familiar workflows, audits and internal compliance expertise. These are real strengths. But the report’s broader message is that digital dependence has raised the standard.

In financial services, identity verification is no longer just about keeping fraud out. It is also about letting good customers in faster.

At PYMNTS Intelligence, we work with businesses to uncover insights that fuel intelligent, data-driven discussions on changing customer expectations, a more connected economy and the strategic shifts necessary to achieve outcomes. With rigorous research methodologies and unwavering commitment to objective quality, we offer trusted data to grow your business. As our partner, you’ll have access to our diverse team of PhDs, researchers, data analysts, number crunchers, subject matter veterans and editorial experts.